In the words of sudden country music sensation Oliver Anthony, “You weren’t born to just pay bills and die.” Yet unless we stop the debt-driven inflation and the Federal Reserve scam used to perpetuate it, we won’t even be able to pay all the bills we work our entire lives to afford.

Inflation is back with a vengeance, despite the quickest rise in interest rates ever and despite the choking off of the M2 money supply. What gives?

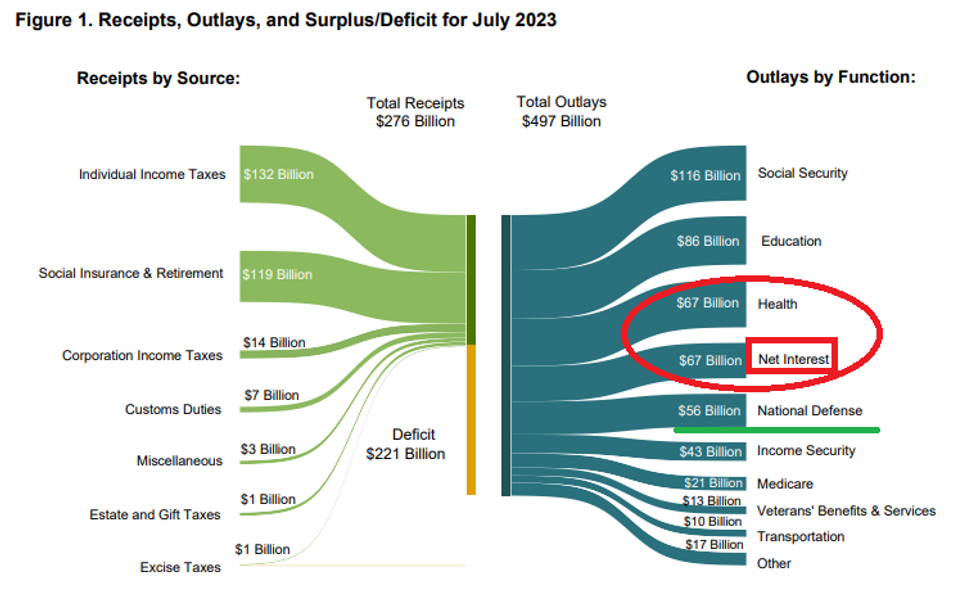

This!

According to the Treasury Department, for the first time ever, spending on interest on the debt not only surpassed military spending in July but tied the cost of our health care leviathan! At $67 billion, the cost of servicing our debt was eclipsed only by Social Security and education (because of student loans) and was 20% costlier than national defense. Put another way, more than 50% of all tax revenue collected from all payroll taxes of all U.S. workers went toward interest on the debt. Headed forward, assuming interest rates aren’t forced up even higher, we will pay an annualized rate of $1 trillion in interest on the debt of government programs and functions that shouldn’t exist even if they were free.

In total, the deficit for July was $221 billion, bringing the total deficit for the first 10 months of this fiscal year to $1.6 trillion. We are now spending 40% more than we did just four years ago. Remember, this is all without an official recession or global war. At this rate of spending, there is simply no number of interest rate hikes that can break the inevitable inflation, and in fact, higher rates now just exacerbate the cost of servicing debt and reinforce the vicious cycle of spending and inflation.

With federal spending outpacing the rate of inflation, it is now creating hyperinflation itself for the first time – without other existential factors.

Headed into the future with $2 trillion annual deficits forever, our government will have to borrow close to $5.5 billion every single day in perpetuity. Over time, this is going to continue to push yields on Treasury bonds higher and higher. As Bloomberg reported last week, the feds had to auction off $103 billion in Treasuries, which was too much for the market to absorb, thereby driving yields on the 30-year Treasury to the highest levels in 12 years.

So where does this leave “we the people” south and west of the Acela corridor?

None of this is natural, flowing from the free market. This is the legacy of venture socialism, defined as politicians, bureaucrats, and the Federal Reserve using government printing presses and regulatory authority to advance the fortunes of a small number of corporate entities at the expense of most American workers. This is the result of gradual policies of debt, regulation, and Federal Reserve monetary morphine for several decades but rapidly accelerating during the 2008 financial collapse and permanently cemented during the COVID policies. It’s a form of neo-fascism without the nationalism.

In order to rectify these policies, we need an immediate budget showdown next month on spending levels and on global warming regulations that make life miserable for consumers.

In addition, Republicans must finally be willing to take on the Federal Reserve and get rid of the ability to tinker with the economy and print money to service this much debt or create asset bubbles. As Thomas Hogan of the American Institute for Economic Research observes, during the 130 years from 1784 until the creation of the Federal Reserve, price levels were essentially flat. During the past 109 years since 1914, however, there has been 3,000% inflation, with most of it occurring since the 1970s, when Nixon took our fiat system off the gold standard.