On one hand, Republicans make a weak case that we shouldn’t reform Medicaid. On the other, there is a Republican bill that pretends that increasing Medicaid spending from $695 billion in 2025 to $847 billion in 2034 (instead of $986 billion) is some massive, fiscally responsible move that we should all applaud without objections. We also have the blue-state Republicans who believe that because their states choose to impose lots of taxes, their high-income residents deserve a tax break.

That’s happening at the same time that the New York Times is raising the alarm about the debt, and it blames both sides. Here is a tidbit:

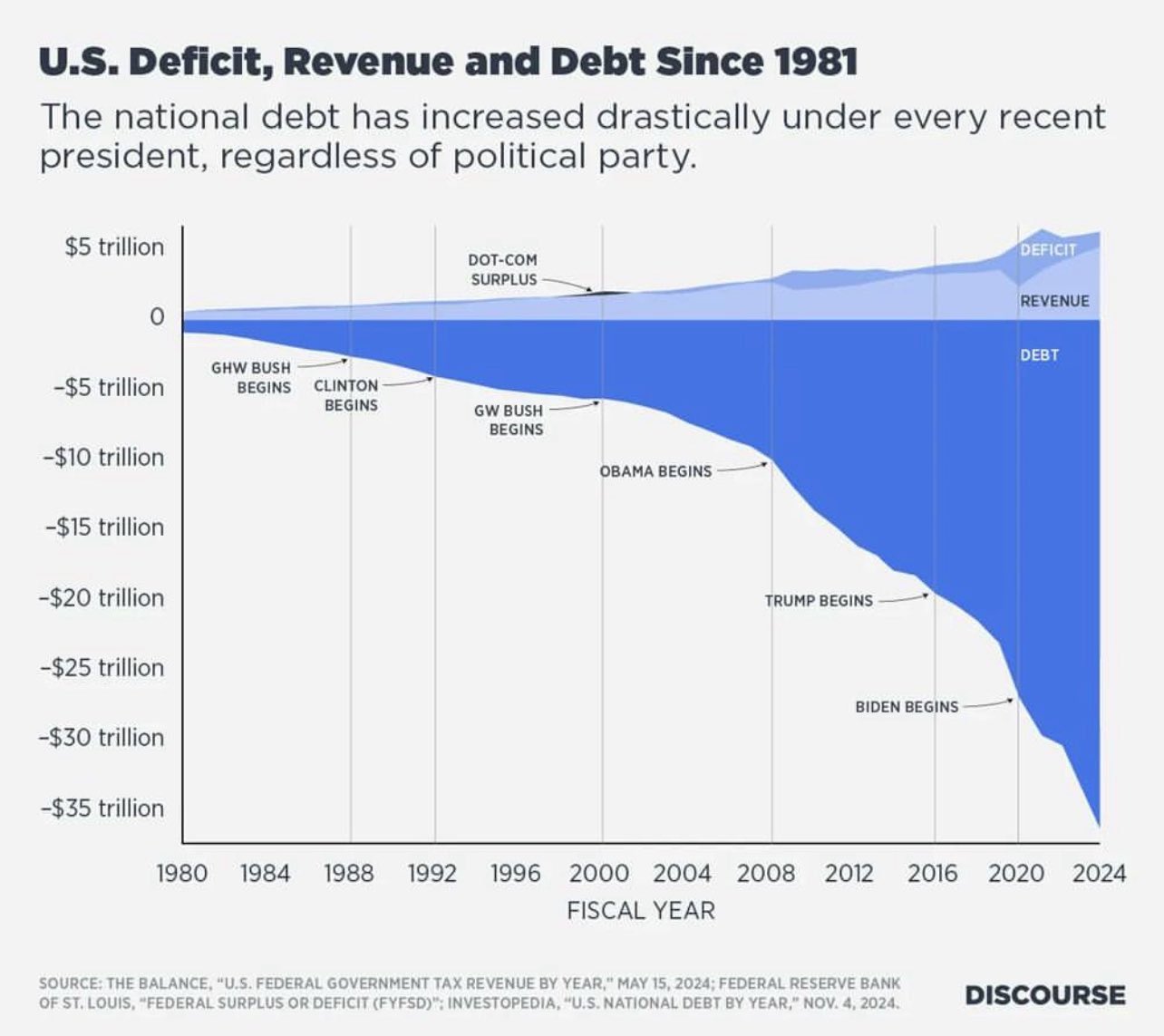

Federal debt has been increasing for years, under both Democratic and Republican presidents. President Trump’s first term was punctuated with the passage of a major tax cut bill and significant pandemic relief spending. The Biden presidency included major deficit spending on a pandemic stimulus bill, infrastructure investment and other legislation. Debt also grew under President Barack Obama and President George W. Bush, largely because of tax cuts, wars and the 2008 financial crisis. The last time the federal budget was balanced, and debts declined, was during Bill Clinton’s presidency.

Notice that Biden is the only president since the budget was balanced who increased the debt like a maniac, even though the country wasn’t really in the midst of an emergency anymore. The other presidents, Bush 43, Obama, and Trump 45, did it under the cover of responding to an emergency.

No doubt, NYT reporters care about the debt now and are willing to raise the alarm because a Republican is in power and pushing for a tax bill. But it is a nice change from when we pretended we shouldn’t worry about the debt because the spending multiplier was so big that all that politically driven government spending would generate significant growth. It is also a nice change from the time when many pretended that interest rates would never go up because the appetite for U.S. debt was infinite, especially from foreigners. Well, that was nonsense, since even if interest rates had stayed low, a small interest rate on a large debt is still very expensive in terms of interest payments. But also, it was not reasonable to assume that interest rates would never go up, considering the scale of unfunded liabilities in our future and the fact that, each time there is an emergency, the debt-to-GDP ratio shoots up.

The world is upside down, but we are still in financial trouble. So, again, I am glad that some in Congress are trying to rein in the spending instead of pretending that any tax bill will bring in tons of growth, meaning we shouldn’t worry about its cost.

Oh, and here is a nice chart that shows that both sides are responsible for this mess.