By Peter Tchir of Academy Securities

The Fed finally cut rates on Wednesday and 2-year yields finished the week higher, 10s didn’t have the decency to rally on Fed day, and according to the Bloomberg WIRP function, the market is pricing in 2.92% by the end of the September 2025 meeting, instead of the 2.84% it had on Monday. So, while the cycle is “new” in terms of actually cutting, with a “surprise” 50 bps, it is difficult to argue that the bond market hasn’t already been pricing this in, perhaps too aggressively!

Stocks were more interesting, as they rallied, faded, rallied, and then faded on Fed day. We then had one of the “crazier” Thursday’s I’ve seen in a while, but on Friday it seemed like we were back to some buying fatigue, though we did have one strong rally off the lows.

{kind=link}

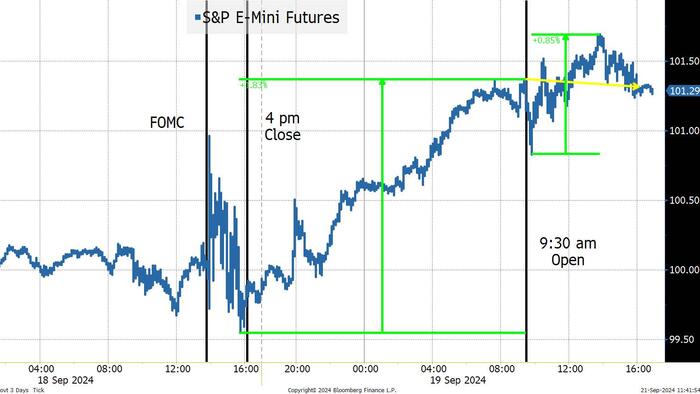

For those of you on Twitter, you might be familiar with Jim Cramer complaining about “pajama” traders. No one seemed to complain about the overnight session driving the show on Thursday as the entire gain for the day came during the overnight session. This chart might be off by a minute or two (not as granular as I would like), but it is clear what happened between 9:30am when the major U.S. exchanges “officially” opened (they all have some element of pre- and post-market trading), to when they closed. The market at best inched higher and probably closed moderately lower. Pretty unusual for an almost 2% up day! That is particularly true of late, when you would expect leveraged ETFs and 0DTE options to amplify the moves – but they didn’t. In a market that has been fraught with often multiple 1% intraday swings (see any number of recent T-Reports), we didn’t even get an intraday “trough to peak” move of 1%! All of that seems weird, and I’m told by some technical traders, that not only was that not constructive, but also the fact that Friday had little volatility and finished lower makes the market precarious, at least from a technical standpoint.

I do suspect that part of the market’s reaction Wednesday night was relief that the Yen didn’t rally (there was concern that a 50 bp move would cause dollar weakness and many still fear the Yen carry trade). Thursday night the Bank of Japan had the opportunity to be hawkish, but they chose not to be, which helped the dollar strengthen against the Yen, but didn’t seem to renew the enthusiasm for the carry trade.

All a bit weird, to say the least.

We sent a lot of information out on the day of the Fed, including Fed Probabilities, where we had our top 2 probabilities as being a “Neutral 50 bp Cut” followed by a “Hawkish 50 bp Cut.” We actually felt that the Fed would try for the hawkish 50 (I think they did), but the market would interpret it as a neutral 50 (because as much as you jawbone, you did actually just cut 50). Our Conclusion Based on a Preponderance of Evidence was that it was somewhere between a neutral and hawkish 50 bps cut, leaving us with two choices on market reaction from our earlier report:

Based on our own pre-FOMC thinking, with a 50 bp cut, we should have been looking to buy the dip. We did not, as the bounce came faster and further than anything we expected (especially after Wednesday’s price action seemed to confirm our view that the market was already positioned too bullishly).

The fact that the rally on Thursday didn’t continue to scream higher is a minor miracle given that we seemed to miss our own takeaways, and Friday’s weakness encourages me to believe that we have yet to see the post-FOMC lows.

Going back to last weekend’s Great Debates, it is interesting to point out that the Philadelphia Semiconductor Index (SOX) finished the week only up 0.4%. AI will still be a driving force in this market, and it did not “catch on fire” like you might have felt it did (it certainly felt like it on Thursday after saying not to buy on Wednesday), but even with that, it wasn’t a particularly memorable week.

So what I think happened:

On the Great Debates:

I’ve been in the “bumpy” landing camp for months. For much of that time I felt I had to push back on the “soft landing” crowd and argue (against consensus) that some industries, sectors, regions of the country, etc., could hit rough patches, while others could do okay. I was arguing, often feeling as though it was pointless, that the job data we were getting out of the NFP Establishment Survey seemed misleadingly strong. However, now we even have Powell climbing on board that bandwagon and questioning the validity of the data in his press conference!

I am happy to present the “bear” case. And I think the economy is far from out of the woods, but I think there is a chance that the economy “muddles” along, causing the Fed to be slow to cut further, while markets are forced to meander along until it becomes clear which direction earnings and the economy are headed. I’m still in the bumpy camp, but I just feel obligated (as an angry contrarian) to point out a few positives (or at least things that aren’t as bad as believed but seem to be getting overlooked):

I think the path to rate cuts will be slower than the market is currently pricing in.

This is the rate that is neither too loose nor too tight in terms of monetary policy. That seems like a pretty important number to me. If I know the neutral rate is X% and the economy is chugging along a bit above trend growth (another important, but possibly mythical number), then the central bank can add 50 bps to X and should get the right amount of cooling. A red hot economy might need X + 1.5%. There are two major problems:

Monetary policy boils down to adding/subtracting Y (a number they don’t really know) to/from X (the Neutral Rate) which they also don’t really know!

The purpose of that rant (aside from making me calm down a bit, as rants seem to be a good way to do that), is that I suspect the Fed will be discussing the neutral rate and the terminal rate much more in the coming months. I assume (probably incorrectly) that the terminal rate the Fed poses as the long-run target rate in their projections should probably be roughly the neutral rate (I think their goal would be neutral monetary policy). Which in turn is probably some guestimate of R* and long-run stable inflation estimates (more wild guesses, but I digress and am starting to hurt my own head).

But, we’ve been running at 5% or higher on Fed Funds since May 2023 and until this month, the Fed didn’t think the economy had slowed enough to dial back? It took the Fed over a year to get to 5%, so initially they didn’t think it was necessary to be that high (nor, I suspect, for that long). What if we didn’t get the slowing, because the neutral/terminal rate should be significantly higher than 2.875%? Maybe we’ve been adding the mythical Y to the wrong X?

The real neutral rate will likely get discussed more and more, since now that the official cutting has begun, we can all switch to debating the timing and size of future cuts, and where will it end.

Without a recession, I expect the neutral rate/terminal rate/R* and other important (but entirely guessed at) factors impacting monetary policy will get more attention.

Moderately higher rates from 2 years on out as we price in a slower Fed, a smaller Fed, and an end point that is higher and takes longer to reach. I think at least 25 bps on 2s vs 10s and think that as we get some more debt ceiling debates, we see the 10-year get back to at least 3.9% with far more risk of moving 50 bps higher than 50 bps lower from here.

Equities. Let’s watch the great AI debate, the election, earnings, and the economy. While I’m nervous that the price action since late Thursday morning gives me confidence that we have an opportunity to buy this market cheaper, remaining small is important when volatility is so high. Adding to disruption, commercial real estate and small caps/value make sense, but again, I think we have to build smaller positions.

On Credit, I feel I’m spending more and more time defending private credit. I like credit as a whole here, as my equity concerns are still more about valuations than economic slowdowns. I continue to think that private credit, for now, is helpful to the overall credit picture and that the debt ceiling debate will once again push investors to be even more overweight credit products at the front end, relative to T-bills (if they can). If you are in the New York area, don’t forget to register here for the October 10th, 5:30 to 7:30pm, Geopolitical and Credit Roundtable led by General (ret.) Spider Marks at Bobby Van’s GCT location.

Lots to digest and I feel awkward pointing out some potential positives on the economy while remaining cautious on equities, but we seem to be in a “good news” is bad sort of environment and positioning is too aggressively long stocks (even with the alleged money on the sidelines, which I think is on the sidelines for a reason and will remain there).

While “officially” the rate cutting cycle has started, don’t get too excited, as it was well telegraphed and is still likely pricing in too much!