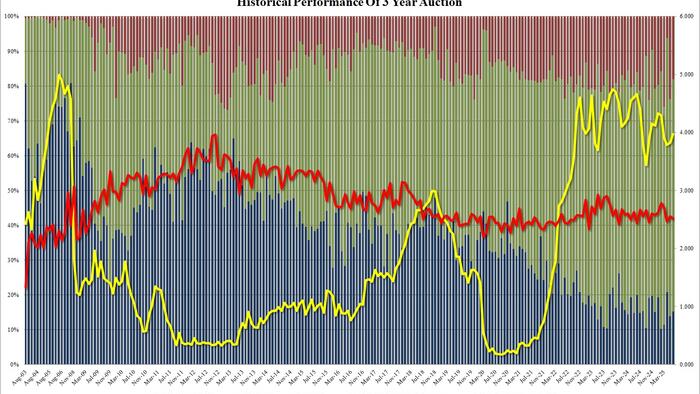

There was some apprehension ahead of today's 3Y auction - the first sale of coupon paper this week - following some very sloppy global auctions around the globe, and certainly ahead of the 10Y and 30Y auctions later this week. In retrospect, the sale of $58BN in 3Y paper came in a bit on the weak side, but hardly enough to spark concerns about prevailing demand.

Just after 1pm, the Treasury announced that today's sale of 3Y paper priced at a high yield of 3.972%, up from May's 3.824% and the highest since February's 4.3%; the auction also tailed the When Issued 3.968% by 0.4bps and was the 7th tailing 3Y auction in the past 9.

The bid to cover was also on the soft side at 2.516, down from 2.556 last month and below the 2.617 six auction average.

The internals were stronger, however, with Indirects rising to 66.8%, up from 62.4% and above the recent average of 66.2%. And with Directs dropping to 18.0% from 23.7%, in line with the average of 18.7%, Dealers were left with 15.2%, also right on top of the six-auction average.

{kind=link}

Overall, this was a mediocre, if smooth, auction, and judging by the lack of market reaction, it was more or less what the market expected. Now attention turns to the balance of this week's auctions which at 10Y and 30Y may be more challenging.