For much of the day, anyone doing analysis on the now-liquidated Silicon Valley Bank was confined to using stale financial data as of Dec. 31... we certainly were when analyzing the impact of SVB's contagion (see here) as excerpted below:

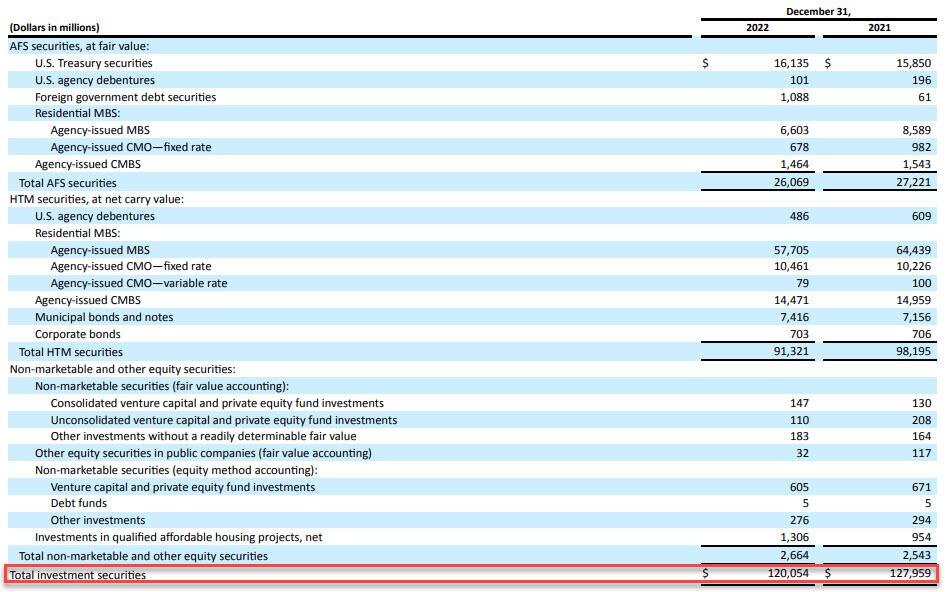

For those who slept through yesterday, here is what you missed and why the US banking system is suffering its worst crisis since 2020. Silicon Valley Bank, aka SIVB, the 18th largest bank in the US with $212 billion in assets of which $120 billion are securities (of which most or $57.7BN are Held to Maturity (HTM) Mortgage Backed Securities and another $10.5BN are CMO, while $26BN are Available for Sale, more on that later )...

... funded by over $173 billion in deposits (of which $151.5 billion are uninsured), has long been viewed as the bank at the heart of the US startup industry due to its singular focus on venture-capital firms. In many ways it echoes the issues we saw at Silvergate, which banked crypto firms almost exclusively.

The big question, of course, is what happened in the past 24 hours to not only snuff the bank's proposed equity offering, but to push the bank into insolvency.

We got the answer just a few moments after that tweet, when the California Department of Financial Protection and Innovation reported that shortly after the Bank announced a loss of approximately $1.8 billion from a sale of investments and was conducting a capital raise (which we now know failed), and despite the bank being in sound financial condition prior to March 9, 2023, "investors and depositors reacted by initiating withdrawals of $42 billion in deposits from the Bank on March 9, 2023, causing a run on the Bank."

As a result of this furious drain, as of the close of business on Thursday, March 9, "the bank had a negative cash balance of approximately $958 million."

At this point, despite attempts from the Bank, with the assistance of regulators, "to transfer collateral from various sources, the Bank did not meet its cash letter with the Federal Reserve. The precipitous deposit withdrawal has caused the Bank to be incapable of paying its obligations as they come due, and the bank is now insolvent."

Some context: as a reminder, SIVB had $173 billion in deposits as of Dec 31., which means that in just a few hours a historic bank run drained a quarter of the bank's funding!

But not everyone got out in time obviously, there is a long line of depositors who are over the $250,000 FDIC insured limit (in fact only somewhere between 3 and 7% of total deposits are insured). The following list, while incomplete, is approximately sorted by size of exposure:

And now the 64 trillion dollar question: was the bank run sparked by the bank's attempted capital raise - which followed a modest $1.8 billion in losses as the bank sold off its AfS holdings to boost its liquidity - or was it the result of an external influence? What we mean by this is that as reported yesterday, several prominent venture capitalists - such as Peter Thiel - advised their tech startups to withdraw money from Silicon Valley Bank on Thursday. Would the bank run have happened if it wasn't for their urging? Or another question: why would some of the VC luminaries actively encourage a bank run? Yesterday we proposed one possible answer.

And while such a course of action by venture capitalists would be understandable, if ethically questionable, what is perhaps more notable is what Bloomberg reported earlier, citing The Infromation: it wasn't just the Peter Thiels of the world:

Prominent venture capitalists advised their tech startups to withdraw money from Silicon Valley Bank, while mega institutions such as JP Morgan Chase & Co sought to convince some SVB customers to move their funds Thursday by touting the safety of their assets.

Let us get this straight: the largest US commercial bank was actively soliciting the clients of one of its biggest competitors, and the 16th largest US bank, knowing full well deposit flight would almost certainly lead to the collapse of a bank which courtesy of fractional reserve banking, had only modest cash to satisfy deposit demands: certainly not enough to meet $42 billion in deposit outflows.

Of course, Jamie, who has suddenly emerged as a key figure in the Jeff Epstein scandal alongside Jes Staley, knows this, and would be delighted with an outcome that kills two birds with one stone: take his name off the front pages and also make JPMorgan even bigger. Actually three birds: remember it was JPM that started that "Not QE" Fed liquidity injection in Sept 2019 when the bank "suddenly" found itself reserve constrained. We doubt that JPM would mind greatly if Powell ended his rate hikes and eased/launched QE as a result of a bank crisis, a bank crisis that Jamie helped precipitate.

And while we wait to see if Dimon's participation in the Epstein scandal will now fade from media coverage, and whether Powell will launch QE, we know one thing for sure: JPM was a clear and immediate benefactor of SIVB's collapse because in a day when everything crashed, JPM stock was one of the handful that were up.