Authored by Peter Tchir via Academy Securities,

Testimony on the hill yesterday turned financials (XLF and KRE) from positive to negative, dragging broader risk markets with them. Overnight, financials are performing well, along with broader risk markets (CDS indices in Europe are particularly strong).

The good news is that the overdone fear of depositor losses seems to be behind us (even after D.C. did little to help on that front yesterday).

I have some ongoing concerns about deposits from an overall yield standpoint (I Know What You Did Last Summer), but that is a concern, that even if I’m correct will work in slow motion.

The overall question of “unrealized bond market losses” (we can include loans and private debt in the “bond market” for these purposes) in the financial system hasn’t gone away, but many are wondering if it is already priced in? I expect that the “unrealized bond market losses” will play out in three ways:

The final issue, one that became quite painfully obvious yesterday, is that the industry has to brace for another round of regulatory scrutiny, brought on to the entire industry by a few particularly egregious situations.

With so many potential things to look at, today we will just revisit a few that have influenced our outlook for the past year so.

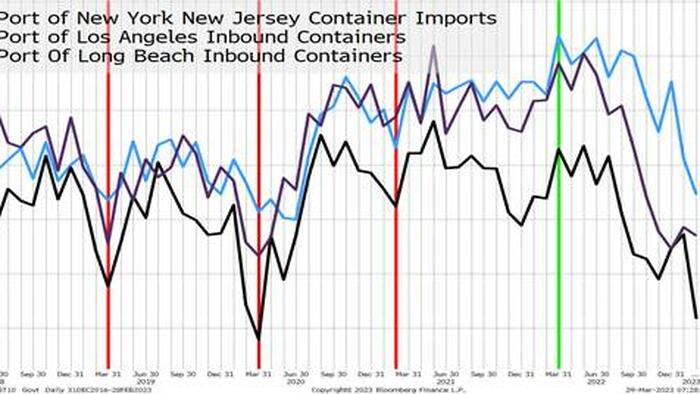

Inventories remain elevated and after some progress, seem to be ticking higher again, which can partly be explained by supply chain resolution, may be better explained by consumer fatigue. We compare total retail inventories with those less autos, just to make sure the automobile industry, which experienced more than its fair share of supply chain issues, isn’t impacting the data disproportionately and it doesn’t seem to be.

A quick look at credit card debt, credit card delinquencies and auto loan delinquencies shows a deteriorating trend (higher debt, higher delinquency frequency), but in most cases still below pre-covid historical averages. Nothing to be overly concerned about today, but the trend is heading the wrong direction for those who are arguing that we can never bet against the American Consumer.

We used 50 day moving averages here (the weekly data is highly volatile and has some serious seasonality (we ramp up pre-holidays, slow down during holidays, etc.). Some of what we are catching in the data may be a typical seasonal effect (though it looks worse than that). It is possible the tragic derailment in East Palestine is affecting the data (I do not have that level of granularity into this data).

For me, it does fit into the “we overordered”, “we have too much inventory” so “we are taking our foot off the gas” narrative that I am using for goods inflation and potential economic impact.

I could look at Baltic Dry Index (which has bounced, but remains in a downtrend) but chose to start trying to figure out what to do with this mess of data from the ports.

{kind=link}

For some reason I couldn’t get the moving average data to work, but in 2017 the lows were in February, for the following years, the lows were in March. So there is some seasonality to them, but:

Given how messy this first cut of data is, maybe it isn’t relevant, but, then again, maybe it is telling us that companies are trying to fix the inventory “glut” (my word) by ordering less?

Remain in a cautious, “risk-off” stance. Positioning doesn’t need to be doom and gloom and trying to time some moves higher and lower makes sense, but I’m erring to side of caution (small short, or small underweight) as laid out in Sunday’s report.

Also, as per Sunday’s “Last Summer” Report, there seem to be more obvious “event risks” to the downside than upside. Yes, that means the market is hedging and preparing for them, but if any of the events materialize (Debt Ceiling, China selling weapons to Russia, etc.) they will still drag markets lower.

The overdone fears of bank deposit safety should be behind us, but now we can all examine the economy again (not liking what I see) and start prepping for earnings which are just around the corner!