After a stellar report from Google and lukewarm earnings from Microsoft, moments ago the 3rd of the tech Megacaps, Facebook, Twitter 2.0, Meta reported Q2 earnings which smashed expectations (despite the debacle that is the Reality Labs division) a result of a record 3+ billion monthly users, but more importantly, provided Q3 revenue guidance that blew away estimates (even as operating expenses are expected to soar while capex is being slashed, in what is hardly an expression of confidence in future growth).

Here is what the company reported for Q2:

Turning to profitability, there was some modest weakness here as profit margin dropped and missed estimates:

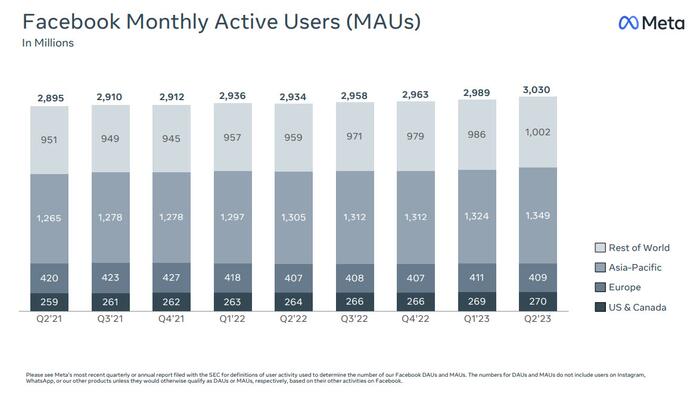

Turning to the company's user base, there was a surprise here: for the first time Meta reported over 3 billion monthly active user:

{kind=link}

Going down the ad side of the business, we find something troubling: Meta's price per ad is slumping, far worse than expected, and the company is making up for this by blasting ever higher ad volumes. In other words, it is cutting prices to keep and raise volumes. But what is the saturation point, and just how many ads can one user see?

And some more ad-linked data:

Turning to expenses we find that while there while there was a modest decline in relative terms, these still remain elevated compared to history.

But while the Q2 results were solid, if concering in that Meta had to slash prices to keep ad volumes, where the market was most impressed was the company's guidance. Here, the company said that it expects third quarter 2023 total revenue to be in the range of $32-34.5 billion, blowing away estimates of $31.18BN. And while the revenue guidance was solid, the surge in expenses largely made up for it:

Additionally, Meta expects its full-year 2023 capex to be in the range of $27-30 billion, lowered from the prior estimate of

$30-33 billion. The reduced forecast was due to "both cost savings, particularly on non-AI servers, as well as shifts in capital expenditures into 2024 from delays in projects and equipment deliveries rather than a reduction in overall investment plans."

This suggests that contrary to expectations of an AI-driven boom, Meta is actually slashing spending, even if it desperately tried to piggyback on the hottest trend around:

The slashed Capex - something one wouldn't do if seeing a clear runway to increased revenue as Meta supposedly does - aren't a surprise: Meta has been cutting thousands of jobs and teams in what CEO Mark Zuckerberg calls its “year of efficiency.” And while Meta has also been investing heavily in artificial intelligence, using the technology to make recommendations — for both content and advertising — more tailored to users’ interests, one would be hard pressed to find that in the cut capex guidance.

In any case, investors were easily fooled that growth for the company with the - don't laugh - 3 billion monthly users will continue apace, and shares surged 4.5% in late trading, trimming an earlier gain of as much as 9%, and bringing the YTD gain to a stunning 158%.

Here is the full Q2 investor presentation (pdf link).