As we enter the last full week of the year, the natural winding down of activity will be punctuated by bursts of activity, centered around the Fed (Wednesday), the BoJ (Thursday) and the BoE (also Thursday) meetings. In terms of data, the highlights are the global flash PMIs today, US retail sales (tomorrow) and inflation prints from the US (PCE on Friday), Canada (tomorrow), UK (Wednesday), and Japan (Friday).

Outside of that, today’s German government vote of no confidence should almost certainly pave the way for a February 23rd election and tomorrow’s CDU/CSU manifesto announcement will help shape the campaign (more later). Another thing to watch is France where Moody’s surprisingly cut France late on Friday night in a rare unscheduled move, albeit one that brings it in line with S&P and Fitch (also more below).

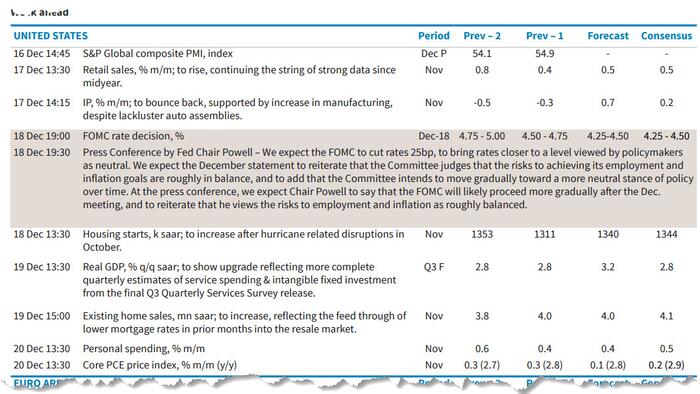

Let’s expand on some of these highlights now and start with the Fed. Our economists’ preview is here but in brief they expect a 25bps cut and then for them to be on hold for the entirety of 2025 as the SEP should show meaningful revisions to the 2024 economic forecasts, with growth and inflation revised higher and the unemployment rate lower. The median dot is likely to show three additional rate cuts but we think Powell will likely deemphasis this signal in the press conference and be as data dependant as he can be. Powell will also likely emphasise that it is still too early for officials to build any major policy changes from the new Trump administration into their outlook. The long-run dot will likely continue its upward migration, rising to 3.1%. Our economists' estimates of neutral are notably above the Fed’s and we think they will likely continue to move this higher.

The BoJ meeting on Thursday is more uncertain, but most economists expect no change and with only a 16% probability of a hike priced in. Our Chief Japan economist previews the meeting here and goes against consensus in seeing a rate hike as the most likely scenario. One of the reasons why a hike might wait until January though is that MP Ishiba is trying to push a stimulus plan through parliament this month and the BoJ may prefer to avoid political interference and delay the hike.

On Thursday our UK economist expects a BoE hold, with a 9-0 vote decision, keeping the rate at 4.75%. The full preview of the meeting is here. The Riksbank is expected to cut rates 25bps on Thursday in a busy last full week of the year for central banks.

For core PCE on Friday our economists believe it comes in a little soft at 0.16% mom versus 0.27% previously with subcomponents in last Thursday's PPI and Friday's import price data, that feed into this number, on the weaker side. However, the year-over-year rate for core PCE should still tick up from 2.8% to 2.9%.

In Germany, Chancellor Scholz's vote of confidence today is scheduled to start at 1:00 pm CET. The expected loss will likely clear the path to early elections on February 23. More importantly tomorrow sees the CDU/CSU publish their manifesto at 11.30 CET. According to current polls the CDU is likely to lead the next government, and the manifesto could give clearer signals on their economic policy priorities, even if the coalition agreement after the elections could result in policy compromises. The key question is whether the CDU will formally signal an openness to reforming the debt brake at this stage. Recently signalled openness by Merz to discuss reforms might just be intended to create optionality for potential compromises in coalition talks. However, a leaked draft of the CDU election manifesto late last week saw a continued commitment to the debt brake which at this stage is not unexpected and corroborates what our economists expected in their preview of this week's events in Berlin here.

Staying in Europe, the Moody’s downgrade of France late on Friday night to Aa3 from Aa2 with a stable outlook was unscheduled and will surprise many when European markets reopen this morning. Their commentary on future deficits is quite damning but the fact that it’s a stable outlook for now, and that this just brings the rating in line with S&P and Fitch, will likely mean that this is more headline grabbing than massively market moving for now. OAT futures are only a little lower in Asia trading. France’s new Prime Minister Francois Bayrou will meet with far-right leader Marine Le Pen and Jordan Bardella (head of National Rally) at 9am CET this morning to start the process of agreeing a budget. So we may see some headlines post the meeting.

For all the rest of the week's events, here is the full day-by-day week ahead courtesy of Deutsche Bank.

Monday December 16

Tuesday December 17

Wednesday December 18

Thursday December 19

Friday December 20

Finally, looking just at the US, Goldman writes that the key data releases this week are the retail sales report on Tuesday and core PCE inflation on Friday. The December FOMC meeting is this week. The post-meeting statement will be released on Wednesday at 2:00 PM ET, followed by Chair Powell's press conference at 2:30 PM.

Monday, December 16

Tuesday, December 17

Wednesday, December 18

Thursday, December 19

Friday, December 20

Source: Deutsche Bank, Goldman, Barclays