After a whirlwind two weeks which saw both the latest FOMC decision and the April jobs report, not to mention the peak of earnings season when all of the top tech companies reported, the calendar takes a quieter turn after the deluge of macro events last week, and the focus shifts on whether markets can continue to find a more solid footing. The latter half of last week saw strong gains for most asset classes thanks to an FOMC meeting that avoided hawkish surprises coupled with a softer payrolls report on Friday that reignited hopes of a soft landing for the US economy. 10yr Treasury yields saw their largest weekly decline of the year so far (-15.5bps) while the S&P 500 posted its best 2-day run in 10 weeks (+2.18%).

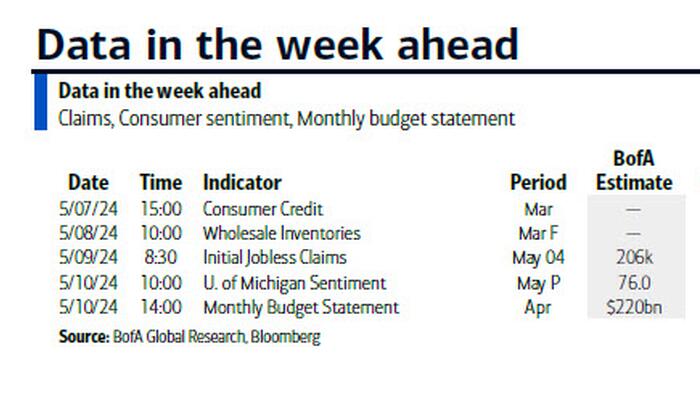

Looking forward, the health of the US economic cycle will remain in focus with today’s Senior Loan Officer Survey from the Fed. The SLOOS has seen a gradual improvement in the past few quarters after the sharp tightening following the regional banking stress last March. A key question is whether the rise in yields since the start of the year could derail the nascent improvement in bank credit conditions. Later in the week, the University of Michigan consumer survey will attract attention on Friday given the recent softening in US consumer confidence indicators.

{kind=link}

The main macro event in Europe will be the latest BoE decision on Thursday. Our UK economist expects this week’s meeting to set the stage for the first rate cut in June and foresees dovish shifts in the MPC’s modal CPI projections and its forward guidance. You can see the full preview here. We will also have the RBA decision on Tuesday (see our economists' preview here), while on Wednesday the Riksbank could deliver the first rate cut of the cycle there. Finally, we’ll have the accounts of April ECB meeting due on Friday. These are unlikely to deliver major surprises, with April's clear if conditional signal of a June rate cut having solidified in recent ECB commentary. But we will watch for any hints on the ECB reaction function beyond June, including on what sort of data might justify consecutive ECB cuts.

The earnings season will begin to taper off this week, with almost 400 of S&P 500 members having already reported. Notable releases will include Walt Disney, Vertex, Uber and Airbnb in the US, Ferrari, Telefonica and Leonardo in Europe and Toyota and Nintendo in Japan.

Day-by-day calendar of events

Monday May 6

Tuesday May 7

Wednesday May 8

Thursday May 9

Friday May 10

Finally, looking at just the US, Goldman notes that the key economic data release this week are the University of Michigan report on Friday. There are several speaking engagements by Fed officials this week, including remarks from Vice Chair Jefferson, Vice Chair for Supervision Barr, Governors Cook and Bowman, and Presidents Barkin, Williams, Kashkari, Collins, and Goolsbee.

Monday, May 6

Tuesday, May 7

Wednesday, May 8

Thursday, May 9

Friday, May 10

Source: DB, Goldman