The week after payrolls is almost always a bit quiet for data and this week DB's Jim Reid reminds us that we have the added kicker of a Fed that has started their media blackout period ahead of next week's FOMC which will be preceded by a key CPI print on Tuesday 13th, one day before the Fed decision.

At the moment markets price in around 22% chance of a hike next week and maybe CPI might be the main thing that shifts those odds towards a hike if the report is strong, according to Reid. If the Fed wants to communicate to the market one way or another ahead of next week then well placed media stories might surface (so far Timiraos has been hinting at a pause/skip).

However before CPI that does seem unlikely as nothing will be 100% decided until then. We are are back to having a fair bit of uncertainly over the near-term Fed outlook though. After spending most of the 4-day shortened week last week rallying around 25bps from the highest point post-SVB, 2yr US notes sold off +16bps on Friday after a strong headline payroll number that seemed to mask some notable weakness under the surface in the report. The headline increased +339k (+195k expected) with +94k of revisions over the last two months. However hours worked ticked down a tenth to 34.3hrs, which marks the lower end of the pre-covid range, and unemployment ticked up three-tenths to 3.7% via the household survey that showed employment falling by 310k with a 440k increase in unemployment. The household part of the report can be more volatile so caution is required. Adding to the confusing nature of the report, average hourly earnings came in at 4.3% YoY (vs 4.4% expected), still too high for comfort for the Fed but ticking lower.

Next up on the agenda, and as we detailed in "Liquidity To Collapse $1 Trillion In "3 Or 4 Months", Pushing Economy Into The Abyss", with the debt ceiling deal signed into law over the weekend, watch for a dramatic rebuild in the US TGA (Treasury General Account) over the next few weeks and months. This starts this week with T-bill issuance that DB’s Steven Zeng suggests could in net terms hit $400bn in June and cumulatively $800bn by the end of August and $1.3tn by year-end. If you’re on the bearish side this deluge could drain liquidity in financial markets but if you’re more sanguine you would say it will just reshuffle money away from money market funds and equivalents (so far no money has left MMFs which are at all time highs).

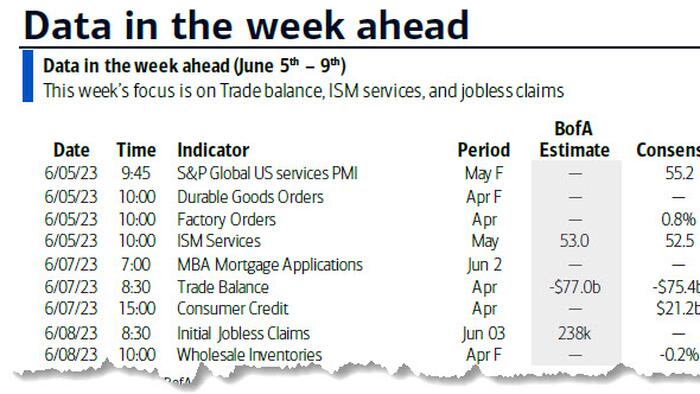

In data terms, the quiet week ahead will be headlined by today's global services PMIs and the US ISM and factory orders prints, both of which disappointed (see here and here). Other highlights will be US factory orders (today) and US trade and consumer credit (Wednesday).

Over in Europe, key data releases for Germany include the trade balance today, factory orders tomorrow and industrial production on Wednesday. Elsewhere in the region, notable releases include the trade balance for France on Wednesday, retail sales for the Eurozone tomorrow and industrial production for Italy on Friday. In Asia, Japanese wages tomorrow and China CPI on Friday will be the highlights.

In terms of central banks, the RBA meet tomorrow with markets pricing in around a 30% chance of a hike with a full hike cumulatively priced in by the August meeting after recent hot inflation numbers. DB economists have now moved to price in a 25bps hike tomorrow, August and September now. The Bank of Canada meet the following day with markets pricing a one-in-three chance of a hike with economists closer to 50/50.

Courtesy of DB, here is a day-by-day calendar of events

Monday June 5

Tuesday June 6

Wednesday June 7

Thursday June 8

Friday June 9

Finally, looking at just the US, Goldman writes that the key economic data release this week is the ISM services report on Monday. Fed officials are not expected to comment this week given the blackout period leading up to the FOMC meeting June 13-14.

Monday, June 5

Tuesday, June 6

Wednesday, June 7

Thursday, June 8

Friday, June 9

Source: DB, Goldman, BofA