Hot on the heels of last week's tech and momentum rout, shaken traders will have to wait until Friday for the main macro event namely the US core PCE print within the income and spending report. Economists expect the core PCE deflator to come in at +0.30% vs. +0.26% last month. This would drop the YoY rate to 2.7%, down from 2.8%, and a level that both Chair Powell and Vice Chair Jefferson suggested that the Fed staff’s estimate had pencilled in.

But while there is nothing big in macro until the end of the week, the same can not be said for corporate earnings, as all eyes will be on earnings with a whopping 178 of the S&P 500 reporting including four of the Magnificent Seven namely Tesla (after Tuesday’s close), Microsoft, Alphabet (Thursday) and Meta (Wednesday). The final three are the 1st, 4th and 6th largest S&P 500 firms by market cap and make up nearly 14% of its market cap. Tesla is down -41% YTD and under a lot of pressure so it’s an important release for them. This all comes off the back of the worst week for the S&P 500 (-3.05%) since the US regional banking stress last March, and the worst week for the Nasdaq 100 (-5.36%) and the Magnificent Seven (-7.73%) since November 2022. A -3.47% decline on Friday marked a sixth day of consecutive losses for the Mag-7.

With three consecutive weeks of losses, the longest such streak since last September, the S&P 500 is now -5.5% from its recent peak. The VIX volatility index rose +1.4 points (and +0.7 points on Friday) to 18.71, to its highest weekly close since last October.

Nvidia (which doesn't report for another month) fell exactly -10% on Friday (-13.59% on the week), contributing around half of the -0.88% loss in the S&P 500 on Friday, and is now down -25% from its highs on 25 March. One catalyst appeared to be their hardware partner Super Micro Computer announcing its earnings date (April 30th) but without preliminary guidance as they have previously tended to do. They fell -23.1%. Everything else related to chips and AI also got stung with Advanced Micro Devices dropping -5.4%, and Arm Holdings -16.9% to 87.19 as examples.

By contrast, the Dow Jones index was largely resilient last week, up +0.56% on Friday and flat (+0.01%) over the week. The Europe STOXX 600 also suffered in the risk-off environment but outperformed the tech heavy US market, falling -1.18% (and -0.08% on Friday).

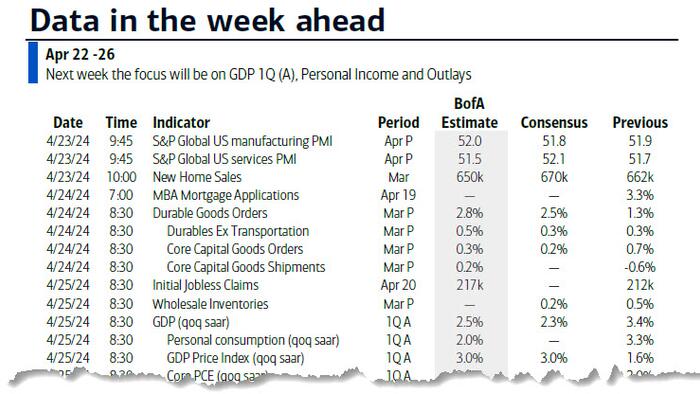

Coming back to this week, the other main highlights by day are the global flash PMIs and US new home sales tomorrow, US durable goods and the German IFO (Wednesday), and US GDP and pending home sales (Thursday).

Alongside the core US PCE print, Friday also sees the latest BoJ meeting and Tokyo CPI. DB's Japan economist expects no change in their monetary policy stance. However, he forecasts that the BoJ will remove its JGB purchasing guidelines from its statement or revise them to make its purchasing operations more flexible. He also sees the central bank raising its inflation forecast for FY24 amid the strong wage growth data already available as of the March meeting.

Elsewhere, the Fed is now on its pre-FOMC media blackout but the ECB speakers will be in full force as you'll see in the week ahead calendar at the end, alongside all the main earnings and macro highlights. 112 Stoxx 600 companies will report this week alongside the 178 for the S&P 500 we mentioned above.

Courtesy of DB, here is a day-by-day calendar of events

Monday April 22

Tuesday April 23

Wednesday April 24

Thursday April 25

Friday April 26

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the durable goods report on Wednesday, the Q1 GDP advance release on Thursday, and the core PCE inflation report on Friday. Fed officials are not expected to comment on monetary policy this week, reflecting the blackout period in advance of the FOMC meeting on April 30-May 1.

Monday, April 22

Tuesday, April 23

Wednesday, April 24

Thursday, April 25

Friday, April 26

Source DB, Goldman, BofA