Markets are starting the week trying to work out what to make of the volatile situation in Russia that saw a remarkable turn late Friday and into Saturday. As DB's Jim Reid speculates, the mutiny and then truce - all within 24-36 hours - means more political instability longer-term than shorter-term although for now there has been virtually no market impact. That said, at one point on Saturday when the Wagner group's Prigozhin had his troops march towards Moscow, it felt that there was a lot of potential global market event risk over the next few days. That has perhaps died down but this whole episode probably increases both the positive and negative tail risks a bit. It could increase the risk of escalation by Putin to reinstate an air of authority, or it could leave him vulnerable which could be seen as positive or negative for Europe, Ukraine and wider markets. It's just impossible to tell at this stage.

Looking forward now, the US PCE (Friday) and Eurozone CPI releases (Wednesday to Friday) are the obvious focal points this week. Also up there in order of importance, the ECB annual forum in Sintra (Mon-Weds) will feature plenty of speakers, including the heads of the Fed, the ECB, the BoJ and the BoE on a panel together on Wednesday.

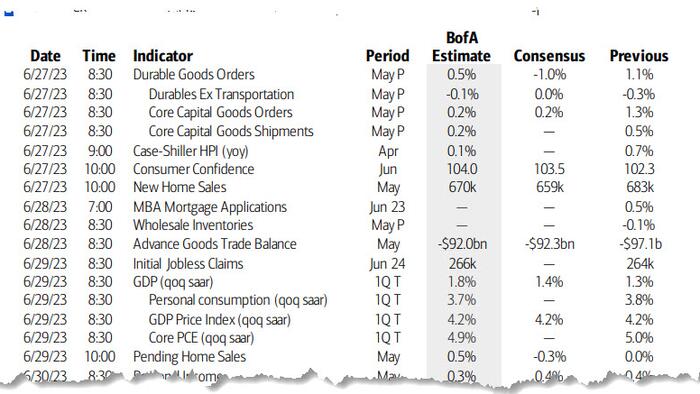

Elsewhere German IFO (which disappointed earlier today), US new home sales and durable goods (tomorrow), results of US bank stress tests (Wednesday), US jobless claims (Thursday), China PMI (Friday), and Tokyo CPI (Friday) are also important with US claims possibly the one to watch most given the recent increase. This increase hasn’t filtered through into continuing claims yet so that is the current shield to worrying about a deteriorating US labour market.

Going through some of the top tier events in a little more detail, let’s start with US PCE on Friday which comes as part of the personal income and consumption report. DB expect the core PCE deflator to soften a tenth on both the monthly (0.3% MoM vs 0.4% last month) and YoY (4.6% YoY from 4.7% last month) readings. Economists point out that to meet the Fed’s forecast of 3.9% YoY core PCE this year we would need around 27bps of monthly prints into YE. DB actually expects 3.6%. All else equal, these prints could be the swing factor between 1-2 Fed hikes out to YE in their own dot plots.

Something that could be interesting is the results of the annual US bank stress tests on Wednesday. Those will be closely watched following the regional banking turmoil this spring that resulted in several bank failures as well as lingering concerns over risks to the banking system tied to deposit dynamics and interest rates. For the first time, the stress test will include an "exploratory market shock component", for the largest banks. The "severely adverse scenario" will focus on the effects of "a severe global recession" coupled with turmoil in real estate markets, both commercial and residential, and corporate debt markets. These stress tests are always a double edge sword. Too onerous and they can create their own turmoil, but too loose and they lack some credibility. So an interesting one to watch.

Later in the week, Italy will kick off European CPI releases on Wednesday, followed by Germany on Thursday with France and the Eurozone on Friday. DB's European economists' inflation chartbook looks at the latest trends and developments here. The team's forecast for the June Eurozone print due on Friday is 5.8% YoY for headline (vs 6.1% in May) and 5.7% for core (vs 5.3% in May). It will be the last set of inflation readings ahead of the July 27th ECB meeting. See the day-by-day calendar at the end as usual for the full week's docket.

Here is a day-by-day calendar of events

Monday June 26

Tuesday June 27

Wednesday June 28

Thursday June 29

Friday June 30

Finally, focusing on just the US, the key economic data releases this week are the durable goods report on Tuesday and the Chicago PMI report on Friday. There are a few speaking engagements from Fed officials this week, including public appearances by Chair Powell on Wednesday and Thursday.

Monday, June 26

Tuesday, June 27

Wednesday, June 28

Thursday, June 29

Friday, June 30

Source: Deutsche Bank, Goldman, BofA