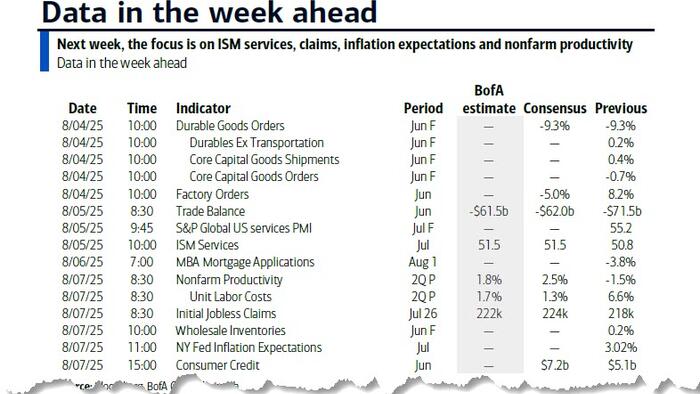

Last week was by far the busiest of the year, with a perfect storm confluence of macro, earnings and central bank newsflow avalanche. Not surprisingly, this post-payrolls week is much quieter; among the US data releases that matter will be Tuesday’s ISM report (forecast at 51.2 versus 50.8 previously), particularly its employment component, and Thursday’s initial jobless claims (225,000 versus 218,000) will be closely watched in light of the payroll revisions.

Tuesday also brings the international trade balance (-$75 billion versus -$71.5 billion), which will include country and product-level details. These will allow for a recalculation of the average tariff rate. DB economists estimate that, as of 7 August, when country-specific rates take effect, the average tariff rate will be 19.6% on a static basis using 2024 trade weights. However, this is likely an upper bound, and after adjusting for overestimation, the more realistic average is closer to 15%. Thursday’s US data also includes productivity (expected at +2.5% versus -1.5%) and unit labour costs (+1.0% versus +6.6%).

In Europe, the highlight will be the Bank of England’s rate decision - DB expects the central bank to cut the Bank Rate to 4%, marking the fifth quarter-point reduction in the current cycle. Additional European data will come from trade and industrial production figures across key Eurozone economies, with Germany’s factory orders due on Wednesday. CPI prints are expected in Switzerland today and in Sweden on Thursday.

In Asia, the focus will be on China’s trade balance, due Thursday, and Japan’s wage data on Wednesday. Chinese exports are expected to slow to 5% year-on-year in July, down from 5.8% in June. The Bank of Japan will release its summary of opinions from the July meeting on Friday and the minutes from the June meeting tomorrow.

On the earnings front, the US season has passed its peak, but notable reports are expected from Eli Lilly, Palantir, and AMD. Other S&P 500 names reporting include McDonald’s, Walt Disney, and Uber. In Europe, attention will be on Novo Nordisk, Siemens, and Rheinmetall. Novo’s report on Wednesday will be particularly interesting following last week’s profit warning. In Japan, Toyota and Sony are set to report. Saudi Aramco, the world’s largest energy company by market capitalization, will release its results tomorrow.

Here is a day-by-day calendar of events

Monday August 4

Tuesday August 5

Wednesday August 6

Thursday August 7

Friday August 8

Finally, looking at just the US, the key economic data release this week is the ISM services index on Tuesday. There are several speaking engagements from Fed officials this week, including an event with Fed Governor Cook on Wednesday.

Monday, August 4

10:00 AM Factory orders, June (GS -4.2%, consensus -4.8%, last +8.2%); Factory orders ex-transportation, June (consensus +0.2%, last +0.2%); Durable goods orders, June final (GS -9.3%, consensus -9.3%, last -9.3%); Durable goods orders ex-transportation, June final (GS +0.2%, consensus +0.2%, last +0.2%); Core capital goods orders, June final (last -0.7%); Core capital goods shipments, June final (last +0.4%)

Tuesday, August 5

Wednesday, August 6

Thursday, August 7

Friday, August 8

Source: DB, Goldman