With the Fed on their media blackout ahead of next week's FOMC, things will be slightly quieter this week in terms of scheduled Fed talking heads and macro events after a hectic round of Fed speak last week including a market rollercoaster sparked by Powell's contradictory comments last Thursday which had a big impact on rates and the curve even if they haven't said much that adds to the debate as to whether the Fed is done and if so, how long they'll stay at these levels. The 2s10s and 2s30s both bear steepened more than 30bps last week (the most since post-SVB) even though 2yr yields were up +1.8bps, and as DB's Jim Reid notes overnight, "although we are fully bought in to the steepener trade I’m struggling to explain why it moved so much last week. Perhaps the long end continues to be hit by supply, US fiscal fears (maybe including extra funding for Israel), and concerns over where the oil price might go whereas the front end is receiving the (relative) flight to quality trade that few want to put on at the long-end." Perhaps the recent back-end moves and the Middle-East tensions are also making the market more comfortable that central banks won’t move again at the front-end even as oil goes higher (for a lenghtier discussion of what is moving yields, see "Morgan Stanley Explains The "Real Drivers" Behind The Rout In Treasuries").

As an aside, Reid cautions that he remains concerned "as to how markets will cope with such high yields at the back end of markets, especially those in the US. We spent 10-15 years with yields and rates low/zero/negative across the DM world, helped by QE as this was seen as the only way we could finance the enormous global debt load. If this synopsis is correct, then surely one of the biggest 2-3 year yield sell-offs in history risks causing a lot of pain beyond any seen so far."

If yields stay elevated, the only way I think I’ll be wrong is if we actually didn’t need those levels of rates and yields in the 2010s, or if central banks and governments have taken on enough of the risk just in time to avoid pain from higher yields. That argument is harder to buy in to with QT and strong government supply combining at the moment. On the risk of accidents it was interesting that the US Regional Bank index fell -3.53% on Friday and is down around -20% since the local peak in August and is less than 10% away from the crisis lows in Q2.

So going back to the calendar, it isn't the busiest week for data but there are a few important signposts which we'll go through below but such is the way of the world it wouldn't be a surprise if the big-tech results have as much impact as the data. This week we get 39% of SPX mkt cap reporting...

... including most of the giga-cap tech names such as Microsoft and Alphabet tomorrow, Meta on Wednesday and Amazon on Thursday, which together make up over $6tn in market cap, and nearly 17% of the S&P 500. Note that the 7th largest in the index Tesla fell -15.58% last week which was a bit of a blow for the mega caps but AI related stocks like Microsoft may fair better.

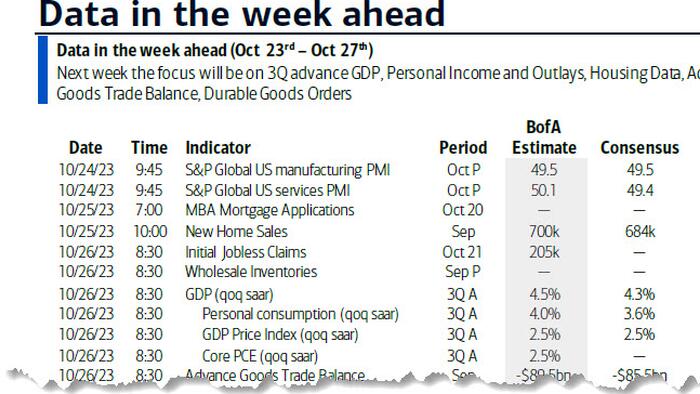

In the US, the data highlight might be the latest US core PCE reading as part of Friday’s consumer income and spending data. Investors will also keep an eye on the preliminary Q3 GDP report in the US where economists expect a 4.3% annualized number (vs. 2.1% in Q2) in what was a quarter that surprised almost everyone with its strength.

Elsewhere in the US we have durable goods orders (DB forecast -0.5% MoM vs +0.1% in August) and advance goods trade balance on Thursday, new home sales on Wednesday, and the final UoM consumer confidence numbers on Friday with the final inflation expectations reading.

In terms of macro events the ECB meeting on Thursday might be a little more dull than it has been for the last 15 months but there could be discussion as to how they will further reduce their balance sheet going forward (see our economists’ preview here). Tomorrow sees the latest quarterly ECB bank lending survey where the recent reports have suggested very tight lending standards but with expectations that this should loosen in the subsequent quarter. This optimism has reduced the concerns over current conditions so we will see if that improvement has materialised and whether it’s expected to continue.

The Bank of Canada will also decide on rates on Wednesday with markets only pricing in around a 10% probability of a hike.

The global flash PMIs tomorrow will also be important, especially to see if manufacturing and Germany can pick up from what are very low levels historically.

There will be more indicators of economic sentiment on the continent next week. This includes consumer confidence for the Eurozone today as well as a gauge for Germany (tomorrow) and France (Friday). Germany will also be in focus when it comes to business sentiment, with the Ifo survey due on Wednesday. In the UK, the focus will be on labour market data tomorrow with unemployment rate already 0.8pp above the lows, the most in the DM world. Moving on to Asia, key data releases in Japan include the Tokyo CPI on Friday and the services PPI on Thursday. This follows news from the Nikkei last night that the BoJ are looking at another tweak to its YCC policy. Our economist continues to believe they'll make changes at their meeting next week.

In terms of earnings, in addition to the US tech earnings mentioned at the top, we have a busy week with the key highlights mentioned in the day-by-day calendar at the end which also includes all the main data and other events.

Day-by-day calendar of events courtesy of DB

Monday October 23

Tuesday October 24

Wednesday October 25

Thursday October 26

Friday October 27

Finally, turning to just the US, Goldman writes that the key economic data releases this week are the Q3 GDP advance release and durable goods report on Thursday, and the core PCE inflation report on Friday. Fed officials are not expected to comment on monetary policy this week, reflecting the blackout period in advance of the FOMC meeting October 31-November 1.

Monday, October 23

Tuesday, October 24

Wednesday, October 25

Thursday, October 26

Friday, October 27

Source: Deutsche Bank, Goldman, BofA