With earnings season now mostly over (AI vanguard NVDA reports on Wednesday) and the economic data slate relatively sparse, the debt ceiling negotiations will dominate this week's calendar. As noted earlier, the latest is that President Biden and House Speaker Kevin McCarthy will meet at the White House today to resume negotiations. There was a slightly more positive tone from both sides after a phone call between the two yesterday. This follows the GOP walking out on talks late Friday. Yellen said over the weekend that the chances that the US can pay its bills by mid-June are "quite low".

Outside of this story, highlights for the week ahead which include the latest FOMC Minutes on Wednesday, the global flash PMIs tomorrow and the US PCE inflation release on Friday. The details of the University of Michigan Survey the same day are going to be interesting as 5-10yr inflation expectations spiked from 2.9% to 3.2% earlier this month in the prelim reading, a level that hasn't been exceeded since 2007. This often gets revised down in the final print but if not, it could mark a firming of inflation at the consumer level. Watch for any upward revisions to Q1 US GDP on Thursday after recent better than expected data. Also on the data front we have UK inflation on Wednesday (last month shocked to the upside at 10.1% - 8.2% expected this week), various sentiment data in Europe and the Tokyo CPI in Japan on Friday.

As DB's Jim Reid notes, from central banks, as the June FOMC slowly comes into view and with an increasing possibility of a hike that was all but ruled out 1-2 weeks ago, there are lots of Fed speakers, especially early in the week (see in the calendar at the end), and also the release of the FOMC meeting minutes on Wednesday. This might help show how high the bar is for the Fed to add more hikes.

Although earnings season is drawing to a close, Nvidia on Wednesday could be worth watching. Nvidia is up +112% in 2023 and has a market cap of $773bn highlighting why AI is becoming a huge topic and one that also moves macro markets. Nvidia is trading on heroic valuations which time will tell if they are justified.

Asian equity markets have shrugged off Friday’s GOP talks walkout losses on Wall Street following comments by President Biden during the G-7 summit that he sees US-China relations improving “very shortly”. Across the region, the Hang Seng (+1.32%) is leading gains with the KOSPI (+0.83%), the CSI (+0.39%), the Shanghai Composite (+0.11%) and the Nikkei (+0.10%) also up. S&P 500 futures (-0.03%) are trading just below flat with 10yr USTs -2.3bps lower, trading at 3.65%, as we go to press.

Early morning data showed that Japanese core machinery orders unexpectedly dropped -3.9% m/m in March (v/s +0.4% expected, -4.5% in February), contracting for the second month in a row. Elsewhere, the People’s Bank of China (PBOC) kept their benchmark lending rates unchanged for a ninth straight month, keeping the one-year loan prime rate intact at 3.65% while the five-year rate, a reference for mortgages, was also held at 4.3%, as expected.

A day-by-day calendar of events, courtesy of DB:

Monday May 22

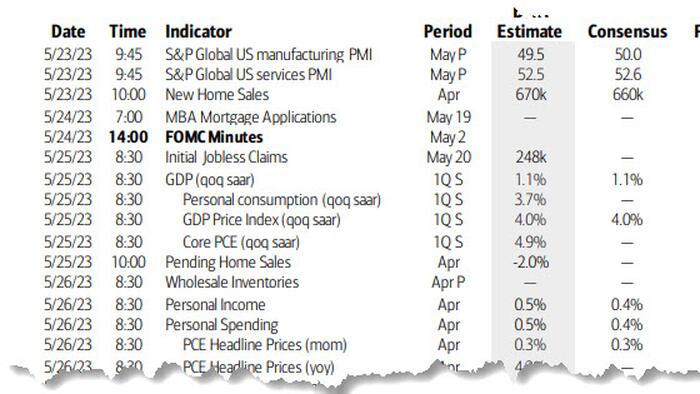

Tuesday May 23

Wednesday May 24

Thursday May 25

Friday May 26

Finally, focusing on just the US, Goldman writes that the key economic data releases this week are the core PCE, durable goods, and University of Michigan reports on Friday. The minutes from the May FOMC meeting will be released on Wednesday and there are several speaking engagements from Fed officials, including governor Waller and presidents Bullard, Bostic, Daly, Logan, and Collins.

Monday, May 22

Tuesday, May 23

Wednesday, May 24

Thursday, May 25

11:00 AM Kansas City Fed manufacturing activity, May (consensus -12, last -10)

Friday, May 26

Source: DB, Goldman, BofA