He may be frontrunning Elon's successful transplanetary efforts by a few years, but in his weekly preview note this morning, DB's Jim Reid writes that unless you've been hiding out on Mars (and if so who could blame you) then tomorrow will shape the direction of the world economy and geopolitics for the next four years. It almost makes the FOMC meeting that concludes on Thursday seem boring by comparison.

We arrive at this monumental election week, the DB strategist writes, with bond markets having been on shaky ground of late with October seeing the worst month for the Bloomberg Global Agg since September 2022 when inflation was only just off its peak, the Fed was still raising by 75bps clips, and the Truss budget and UK LDI pension crisis had exaggerated the sell-off. Last week 10yr US yields rose +14.4bps with +10bps of it on Friday and a little surprisingly after a soft, albeit weather impacted, payrolls report. The most impressive part of last week's price action though was that it occurred alongside prediction markets pulling back from the Red sweep expectation that peaked the previous week. As an example, last weekend Trump has a probability of 61% on PredictIt versus 52% on Friday and 48% on Saturday while slightly rebounding this morning to currently stand again at 51%. On Polymarket.com Mr Trump was as high as 67% on Wednesday but this dropped to around 59% on Friday and over the weekend fell to as low at 53% (currently 58%), with a Republican sweep now at 39% having been as high as 49% last Tuesday. The dip over the weekend came after a highly anticipated Selzer De Moines Register Iowa poll was released on Saturday. The poll saw Harris with a 3-point lead in a state where polling averages have Trump 9 points ahead. Many political commentators had been waiting for this poll as it has one of the best track records amongst pollsters with FiveThirtyEight describing Selzer as "the best pollster in politics".

Anyone who has read "Fooled by Randomness" will be aware of Nassim Taleb's view that its often difficult to assess the difference between luck and skill when it comes to someone with a good track record. Someone always has to have the best track record. That could be skill or it could be say choosing heads five times in a row and getting it right. In response, Treasuries are sharply higher, with all of Friday's losses reversed, as the 10Y yield . The dollar index, which has been correlated to some degree with a Trump victory, is down just over half a percent and flirting with the largest drop in two months.

Ahead of the vote, DB's US economists have published a note which provides a comprehensive overview of the "swing states" that will decide the election, and note that while a winner is likely to be declared in MI, AZ, WI and NV within the first 24 hours of the polls closing on Tuesday, PA and GA are likely to take longer to assess – potentially 3-4 days or longer if there are recounts. If states are disputed, we may not know until December 11, which is the federal deadline for states to certify their electors. So there remains a large degree of uncertainty around both the result, including the very tight House race, and when we will know it.

Turning away from the elections, on Thursday, when we may or may not know who the next President is going to be, we should almost certainly see a 25bps cut from the Fed and a reiteration from Powell that the Fed's subsequent meetings will be data dependent. This potential cut is likely to be unanimous but subsequent meetings could easily be less so. The data dependency will mean it might be tough to garner too much from the meeting, especially if the election outcome and with it future fiscal and trade policies are unknown. Even if the election outcome is known the full extent of policy change could take months to become apparent, especially on trade if Trump wins.

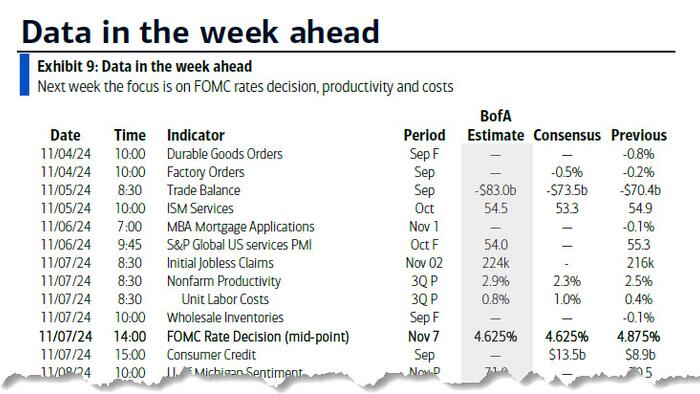

The rest of the week's events they'll pale into insignificance versus the above. However, the brief day-by-day main highlights outside of this include US factory orders and a 3yr UST auction today; China's Caixin services ISM, the RBA meeting, US ISM services and a 10yr UST auction tomorrow; German factory orders, Eurozone PPI and a 30yr UST auction on Wednesday; German industrial production, Eurozone retail sales, US productivity, claims and unit labour costs, alongside BoE, Riksbank and Norges rate decisions on Thursday; with the UoM consumer survey on Friday.

In China, the focus will be on the Standing Committee of the National People’s Congress meeting expected to be held today through Friday as investors seek more details on stimulus measures. A fiscal stimulus package could be announced after the meeting on Friday. For the BoE, economists expect the central bank to make a quarter point cut for the second time this cycle, taking Bank Rate to 4.75%. He also highlights that the BoE's projections that are also due next week will incorporate this week's Autumn Budget (our economist breaks it down here).

After last week's juggernaut, Q3 earnings slow down substantially but we will have several marquee names reporting, including Vertex Pharmaceuticals, Palantir, Constellation Energy, Zoetis, Marriott, NXP Semiconductors, Diamondback Energy, Ferrari, Apollo, Novo Nordisk, Toyota Motor, Qualcomm, ARM, Gilead Sciences, Arista Networks, Airbnb, National Grid, Fortinet, Block, Sony, Paramount and some more.

Day-by-day calendar of events

Monday November 4

Tuesday November 5

Wednesday November 6

Thursday November 7

Friday November 8

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the ISM services report on Tuesday and the jobless claims report on Thursday. The November FOMC meeting is this week. The post-meeting statement will be released at 2:00 PM ET, followed by Chair Powell’s press conference at 2:30 PM. Election Day is on Tuesday, and states will report results over the course of the night.

Monday, November 4

Tuesday, November 5

Wednesday, November 6

Thursday, November 7

Friday, November 8

Source: DB, Goldman