The week after payrolls is usually quiet but as DB's Jim Reid notes, because the first Friday of the month being the latest it could possibly be this month, we go straight into US CPI (Wednesday) week, with PPI (Thursday) for an added bit of inflationary sparkle. Outside of this the main highlight will be Powell's semi-annual monetary policy testimony before the Senate Banking Committee (tomorrow) and the House Financial Services Committee (Wednesday). The latter comes after CPI which will possibly spread the interest level over the two appearances rather than most of the focus being on the first as per usual. Elsewhere in the US, watch out for the NY Fed inflation expectations series today after a stronger equivalent from the University of Michighan survey just before the weekend on Friday. After that we wait until this Friday for the other important US data, namely retail sales and industrial production.

In Europe we have the UK Q4 GDP reading on Thursday following last week's BoE meeting (our UK economist's recap is here). Elsewhere in the region, January CPIs are due in Denmark and Norway today, and Switzerland on Thursday. In terms of earnings we have 75 S&P 500 companies and 79 Stoxx 600 companies reporting.

The tariff news will clearly continue to dominate the agenda all week, especially after Mr Trump announced on Friday that he'd be holding a press conference early this week on the US plans for equalizing tariffs on "reciprocal trade" with an added mention for autos. Then on Air Force One last night Mr Trump said he would put 25% tariffs on steel and aluminium imports later today. Canada, Mexico and Latin America would be the most impacted given that's where the US imports most of these goods from.

Looking forward now and in terms of Powell's testimonies this week, the overarching message is likely that the Fed is not in a hurry to cut rates at the moment, with Friday's payrolls and to a lesser extent the UoM inflation expectations series the latest support to that message. Even though headline (+143k) and private (+111k) payroll gains were below expectations, net upward revisions of 100k over the prior two months, a decline in the unemployment rate to 4.0% (4.1% expected), and average hourly earnings +0.5% on the month (vs. +0.3% expected), made it a hawkish report.On top of that, the annual benchmark revision to the level of March 2024 nonfarm payrolls (-598k final vs. -818k preliminary) was not as large as the BLS had previously projected. See our economists' US employment chart book here for everything you wanted to know about the labour market post this release.

For those inflation expectations last Friday the 1yr level was up to 4.3% (expected 3.3%) and the more important 5-10yr one at 3.3% (expected 3.2%). If confirmed in the final reading the longer-term expectations have only been higher for one month (June 2008) since 1995. This series continues to be ridiculously partisan post the election though with the 1-yr number seen around 5% from Democrat supporters and around zero for Republicans. So how reliable this number is at the moment is open is debatable.

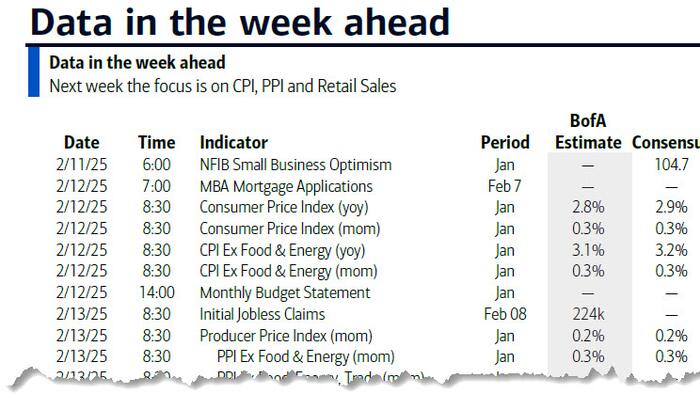

Finally, talking of inflation, strong seasonally adjusted gains in food and energy prices should keep headline CPI (+0.31% forecast vs. +0.39% previously) above core (+0.28% vs. +0.23%). YoY headline CPI should remain roughly steady at 2.9%, while that for core would just round down to 3.1%. OER will continue to be a big focus. For PPI it‘s as ever the components that go into core PCE that will gain all the attention.

Courtesy of DB, here is a day-by-day calendar of events

Monday February 10

Tuesday February 11

Wednesday February 12

Thursday February 13

Friday February 14

Finally, according to Goldman, the key economic data releases this week are the CPI report on Wednesday and the retail sales report on Friday. There are several speaking engagements from Fed officials this week, including Chair Powell's semi-annual Congressional testimony on Tuesday and Wednesday.

Monday, February 10

Tuesday, February 11

Wednesday, February 12

Thursday, February 13

Friday, February 14

Soruce: BofA, Goldman