The French snap election on Sunday (part one) will be the main event this week with weekend opinion polls showing support for Le Pen's National Rally continuing to edge up with the latest poll of polls showing support at 33%, versus the 27% for the far-left New Popular Front (NPF) and 20% for Macron’s movement. As an interesting aside, DB's Jim Reid notes that one of the NPF members Eric Coquerel, who was chair of the finance committee prior to the dissolution of parliament two weeks ago, said that his party's alliance would raise the top marginal rate of income tax to 90% if it were elected. The top rate is currently 45%. While the constitutional court may well prevent this if they were in power, it is more evidence of the potential consequences of this election.

Staying with politics, it will also be fascinating to see the first televised debate between Biden and Trump on Thursday evening in the US. There is plenty of scope for big headlines and for the candidates to gather some momentum or see it go into reverse.

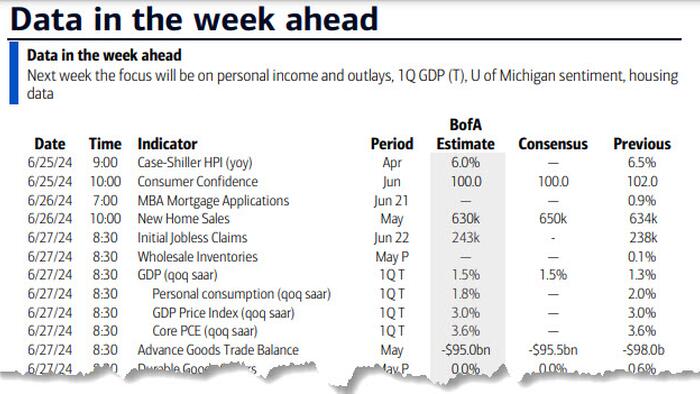

In terms of data the main event is Friday's US core PCE. Friday is also a big day for inflation in Europe where we get the flash CPI shortly after the Tokyo CPI in Japan is released earlier in the day.

Other highlights this week by day are the German IFO today; US consumer confidence, Japan PPI, Canadian CPI tomorrow; US new home sales, Australia CPI and a 5yr UST auction on Wednesday ; US trade, durable goods, and a 7yr UST auction on Thursday; and with Friday bringing German unemployment, and the final UoM US consumer sentiment alongside the inflation data mentioned above. The day-by-day calendar at the end gives a fuller dairy of events.

Previewing Friday's US core PCE deflator, DB's economists believe it should increase +0.17% (vs. +0.25% previously), which would have the effect of lowering the year-over-year rate by 12bps to 2.63%. One note of caution is that their estimate does not include the -10.2% plunge in the seasonally-adjusted PPI for international scheduled passenger air transportation. Their estimate would be about 5bps lower if the BEA does not smooth through this drop. Thus, risks are skewed to the downside which is certainly one to watch.

Moving on to European inflation, our European economists' inflation previews Friday's flash releases here.They expect Eurozone HICP to come in at 2.40% YoY (2.57% in May). Across countries, their forecasts are 2.4% (2.8%) for Germany, 2.5% for France (2.6%), 0.8% for Italy (0.8%), and 3.4% for Spain (3.8%).

Another thing to watch is Nvidia and tech. Nvidia became the largest company in the world on Tuesday night before Wednesday's holiday. It then opened over 3% higher on Thursday. However from this peak it fell around -10% into Friday's close. Is this a brief hiccup, or the start of some air being let out of the ballon?

On the earnings front, investors will be looking at the latest reports from Fedex (Tue), Micron (Wed) and Nike (Thu).

Courtesy of DB, here is a day-by-day calendar of events

Monday June 24

Tuesday June 25

Wednesday June 26

Thursday June 27

Friday June 28

Finally looking at just the US, Goldman notes that the key economic data releases this week are the durable goods report on Thursday, and the core PCE and University of Michigan reports on Friday. There are several speaking engagements from Fed officials this week including Governor Waller on Monday and New York Fed President Williams on Sunday.

Monday, June 24

Tuesday, June 25

Wednesday, June 26

Thursday, June 27

Friday, June 28

Source: DB, Goldman, BofA