With 178 S&P companies (including the biggest tech mega caps) representing a third of the index, and some 40% of index earnings, slated to report Q1 results this week, all eyes will be on the busiest week of earnings season, but there is plenty more to keep investors busy.

Before we focus on earnings, let's take a look at the barrage of econ data on deck, summarized conveniently by DB's Jim Reid. In the US Q1 GDP, the employment cost index (ECI), core PCE, and consumer confidence are the highlights with us now in the Fed blackout period ahead of next week’s FOMC. Meanwhile, we will see inflation and growth data in the Eurozone, and the BoJ's decision in Japan on Friday where DB has a non-consensus call (more below). Big tech (14% of S&P in 4 names), pharma and oil earnings will fill out a busy earnings week. Watch out for First Republic Bank reporting as well after the closing bell today.

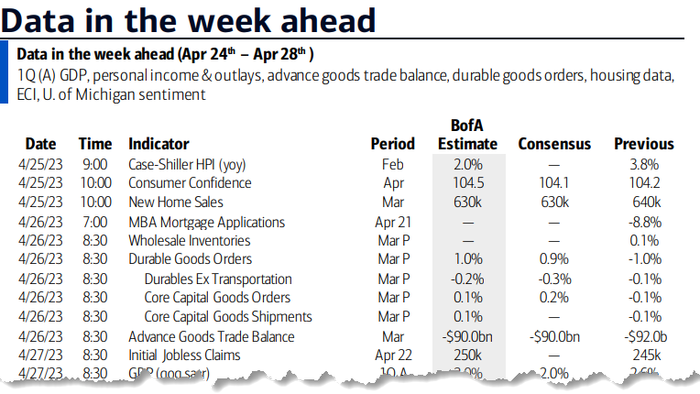

If we start in more detail now with the US, most of the key data is on Thursday and Friday. Before that tomorrow’s new home sales and consumer confidence are also important, especially the latter. The first reading of Q1 GDP is out on Thursday and economists expect a +2.0% print, versus +2.6% in the last quarter of 2022 with consumer spending (+3.7% vs. +2.5%) leading the way. However, Friday’s personal consumption and income data for March may well show that the bulk of the consumer boom in Q1 was in January and February due to warm weather. Within that report on Friday, the latest core PCE deflator will be a key report alongside the ECI. These will be the last big inflationary datapoints ahead of the FOMC.

In Europe, growth and inflation data is due for key economies on Friday. These include GDP and CPI releases for Germany and France and GDP for the Eurozone. There will also be a plenty of sentiment gauges for the bloc. These include the Ifo survey for Germany today, consumer confidence for Germany and France on Wednesday and a list of metrics for Italy and the Eurozone on Thursday.

Over in Asia, all eyes will be on Japan with both the BoJ decision and lots of key data including Tokyo CPI, labor market, retail sales and industrial production indicators all due on Friday. Our Chief Japan economist previews the central bank meeting, the first one for the new Governor Kazuo Ueda, here. Against the market consensus, he expects the BoJ to undergo a policy revision on the back of inflation risks, with potential outcomes including the termination of YCC, strengthening of forward guidance on short-term rates, and greater flexibility of JGB purchasing operations. For data releases, our economist expects unchanged unemployment and Tokyo CPI and a -0.4% MoM fall in industrial production (see full preview here).

Earnings season continues apace this week, with Big Tech reporters taking center stage (we will have more to say in a subsequent post_. Comprising almost 14% of the S&P 500 by market cap, Microsoft and Alphabet tomorrow, Meta on Wednesday, and Amazon on Thursday will be among the most anticipated reports. The only one missing from the pack is Apple, which will report on May 4th. Other notable tech earnings this week include Texas Instruments (tomorrow), SK Hynix (Wednesday), Intel (Thursday) and Sony (Friday).

In Europe the focus will be on key banks, including Credit Suisse (today) and UBS (tomorrow). The former will clearly be interesting given all that went on in Q1. Outflows will be worth watching just to see how serious the situation was at the time. In Asia, a number of Chinese banks report throughout the week. Meanwhile in the US, investors will be laser focussed on First Republic which report today. After trading in a 120-150 range in the first 2 and a bit months of the year, they have been in a 12-15 range over the last month. So they haven't broken back out of their depressed range but haven't deteriorated further. So these results could be important to the company and wider sentiment as this has been the perceived next weakest link.

There are also some pharma heavyweights reporting, including Novartis (tomorrow), AstraZeneca and Sanofi (Thursday) in Europe. In the US, we'll hear from Eli Lilly, AbbVie, Merck and Bristol-Myers Squibb (Thursday), among others.

Consumer demand will be gauged from an array of earnings from companies including McDonald's, Chipotle, PepsiCo (Tuesday), Coca-Cola (today), Domino's, Mondelez (Thursday) and Hilton (Wednesday). In autos, the focus will be on BYD (Thursday), Mercedes-Benz (Friday) and GM (Tuesday). Investors will be particularly interested in EV rollouts and pricing. Among other economically-sensitive bellwether stocks, industrials reporting include UPS, Raytheon, General Electric (Tuesday), Honeywell, Caterpillar, Northrop Grumman (Thursday) and Boeing (Wednesday).

Courtesy of DB, here is a day-by-day calendar of events

Monday April 24

Tuesday April 25

Wednesday April 26

Thursday April 27

Friday April 28

Finally, taking a closer look at just the US, Goldman writes that the key economic data releases this week are the durable goods report on Wednesday, the Q1 GDP advance release on Thursday, and the employment cost index and core PCE reports on Friday. Fed officials are not expected to comment on monetary policy this week, reflecting the FOMC blackout period.

Monday, April 24

Tuesday, April 25

Wednesday, April 26

Thursday, April 27

Friday, April 28

Source: DB, Goldman, BofA