After last week's non-stop rollercoaster, it will be a quieter week ahead for global macro with perhaps the most interesting event of the week being Nvidia's earnings on Wednesday. The company always reports a couple of weeks after the main stretch of US earnings season is over so it will act as a potent "digestif" to Q1 reporting. As DB's Jim Reid reminds us, this time last year the mainstream AI frenzy began around the time of Nvidia's results where the company climbed over 20% on results day and has now tripled in value over 12 months.

Staying in the US, the FOMC minutes on Wednesday are likely to be the main economic event however, it’s unlikely to contain much new material especially since the meeting we have seen CPI and PPI. Perhaps the busy week for Fedspeak will prove more interesting. Vice Chair Jefferson today and Governor Waller tomorrow are early week highlights with the rest in our day-by-day week ahead at the end as usual. In all, there are a whopping 16 Fed speakers this week. Lagarde and the BoE Bailey speak tomorrow.

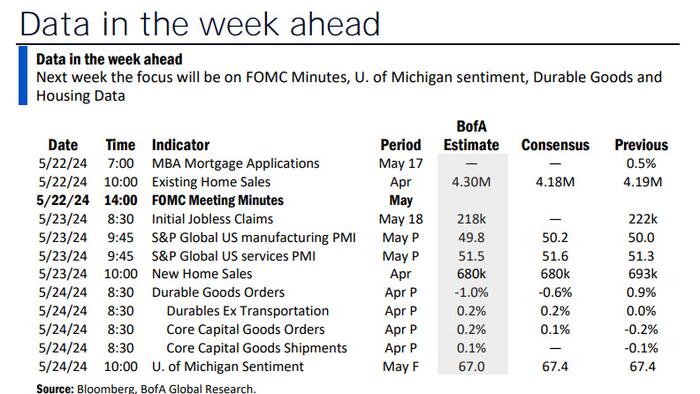

In terms of US data, notable releases include durable goods orders (DB forecast +0.5% in April vs +2.6% in March) and the final reading of the University of Michigan's survey on Friday, as well as housing market data throughout the week. For the UoM survey, inflation expectations will be a highlight as the preliminary reading showed short- and longer-term expectations edging up. The survey is currently transitioning from 100% phone to 100% web-based responses over a 4-month period. So strange or inconsistent readings are possible.

{kind=link}

The global flash PMIs on Thursday will be a highlight alongside UK inflation on Wednesday and retail sales and consumer confidence on Friday. DB's UK economist expects the headline to drop to around 2.2% YoY, 18 months after peaking at 11.1%. He sees core CPI at 3.6% and services at 5.4%, both also down. He sees risks to the headline projection as skewed to the downside. Canada's CPI is also out tomorrow.

In Germany, PPI tomorrow and the breakdown of Q1 GDP on Friday, are likely the main events in mainland Europe. In Asia, the national CPI in Japan on Friday is the main release. Our Chief Japan economist expects core inflation ex. fresh food to be up 2.2% YoY (2.6% in March) and core-core ex. fresh food and energy up 2.5% (+2.9%), both rising +0.1% on a seasonally-adjusted MoM basis.

Courtesy of DB, here is a day-by-day calendar of events

Monday May 20

Tuesday May 21

Wednesday May 22

Thursday May 23

Friday May 24

Finally, turning to just the US, the key economic data releases this week are the existing home sales report on Wednesday, the durable goods orders report and the University of Michigan report on Friday. The minutes from the May FOMC meeting will also be released on Wednesday. There are several speaking engagements from Fed officials this week, including remarks from Vice Chair for Supervision Barr, Vice Chair Jefferson, Governor Waller, and Presidents Bostic, Mester, Barkin, Williams, Collins, and Goolsbee.

Monday, May 20

Tuesday, May 21

Wednesday, May 22

Thursday, May 23

Friday, May 24

Source: DB, Goldman, BofA