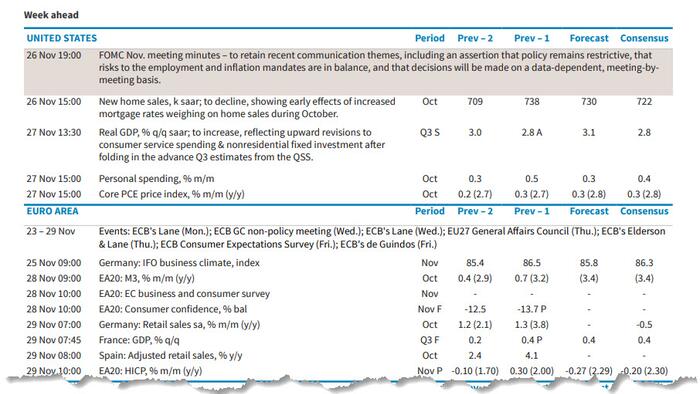

We start what DB's Jim Reid says should be another relatively quiet week ahead with Thanksgiving Day on Thursday, which is why he expects whatever action we have this week to be packed into the early part of it. On that front US core PCE on Wednesday will be the highlight with durable goods the same day. The minutes of the last FOMC come out the night before so that will also be interesting given the meeting started the day after the election with the result known. On the same day November US consumer confidence will also be interesting given the election. It is expected to climb but the UoM consumer sentiment reading on Friday dipped a little although the headline stat from the report was that 5-yr inflation expectations hit 3.2%, only matched in one month since the pandemic (November 2023), and before that you'd need to go back to 2011 to see the last time we were at 3.2%. The other main global highlights are the flash November CPIs in Europe on Thursday/Friday and the Tokyo CPI in Japan the day before.

Looking at more detail into the core US PCE deflator, DB expects +0.29% vs. +0.25% last month which if correct would take the YoY rate from 2.65% to 2.81%. The second print of Q3 GDP (no change at 2.8% expected) on the same day could risk some revisions to PCE inflation, so there is some uncertainty. Clearly this release will have implications for what is proving to be a tight decision in December as to whether the Fed will cut. At the moment the market is pricing in a 60% probability.

Linked into Fed pricing, the market is reacting constructively to the nomination of Scott Bessent for Treasury secretary. This was announced late on Friday (after the US close) and basically takes us back to the direction of travel just over a week ago before various other candidates skipped ahead in the market's pricing. On Polymarket.com he was as high as a 89% probability on November 12th and as low as 11% last Wednesday and still 14% at the lows on Friday. Bessent, a hedge fund CEO, is known to be a fiscal hawk so this should ease some of the more extreme deficit fears as he has advocated a 3% deficit by 2028. In practice that will be extremely tough but for now the market can be a bit relieved. He is also thought to be less extreme on trade policy than some of his rivals for the job. He has recently been quoted in the FT suggesting Trump's tariff policy position could be changed after negotiations with various countries, and he has previously told CNBC that "I would recommend that tariffs be layered in gradually". We will see how influential his views will be on this front. Remember a week ago Elon Musk suggested that appointing Bessent would be a disappointment as it would amount to "business-as-usual". The market will probably be more appreciative of this trait for now. This morning yields on the 10yr US Treasuries are 10bps lower, while the S&P is +0.5%higher. The dollar is around -0.6% lower and base metals are generally higher although gold (-1.6%) has lost some of its risk premium after a good rebound last week.

Reverting back to the other highlights this week. For the flash European inflation prints for November, which start on Thursday with Germany, with the French, Italian and Eurozone-level print following on Friday, our European economists detail their expectations and recent trends in data here. They see Euro Area HICP accelerating to 2.27% YoY (2.0% in October), with country-level forecasts including 2.63% for Germany, 1.66% for France and 1.27% for Italy. Other notable data in key Eurozone economies includes the Ifo survey (today) and retail sales in Germany (Friday) as well as consumer confidence in Germany and France on Wednesday. Q3 GDP numbers are also due in Canada, Sweden and Switzerland on Friday. In Asia, indicators to watch include industrial profits in China and October CPI in Australia (DB forecast 2.4% YoY vs 2.1% in September) on Wednesday. The rest of the day-by-day calendar is at the end as usual.

Courtesy of DB, here is a day-by-day calendar of events

Monday November 25

Tuesday November 26

Wednesday November 27

Thursday November 28

Friday November 29

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the durable goods report and core PCE inflation on Wednesday. The minutes from the November FOMC meeting will be released on Tuesday. Fed officials are not expected to speak this week.

Monday, November 25

Tuesday, November 26

Wednesday, November 27

Thursday, November 28

Friday, November 29

Source: DB, Goldman,Barclays