Buckle up as we have 48% of S&P’s market cap reporting this week not to mention the Fed (Wednesday afternoon), ECB (Thursday morning), and BOJ (Thursday night/Friday morning).

The big event will be the 11th, and according to DB's Jim Reid and most other banks, final, Fed hike of this cycle on Wednesday. However the ECB (Thursday) and BoJ (Friday) meetings are also big events. In a busy week, some other highlights include the global flash PMIs today, the ECB bank lending survey (tomorrow), US Q2 GDP (Thursday), US core PCE, US ECI alongside German and French CPI (all Friday).

In terms of earnings, big tech, oil majors and notable semiconductor firms will be the highlights with 165 S&P 500 and 200 Stoxx 600 companies reporting this week. Watch out for Microsoft, Alphabet (tomorrow) and Meta (Wednesday) after some slightly disappointing tech earnings last week.

Going through the three big central bank meetings and other highlights in more detail now.

The Fed will almost certainly hike +25bps on Wednesday which the market expects to be the final hike in the cycle. A September hike is priced at 33%, albeit up from 22% the previous week. With two CPIs and payrolls to come before then there is plenty of incoming data to confirm or dispute that assumption. The key for this meeting is if and how much the Fed messaging changes given recent softer inflation data. DB economists suggest that there is little downside at this stage for the Fed to do anything other than maintain a hawkish bias even if they acknowledge the progress.

Over in Europe, the ECB will also decide on rates on Thursday. The ECB is expected to deliver a +25bps hike, taking the deposit rate to what DB economists see as a terminal level of 3.75%, even if they see a hike in September as a genuine possibility. Aside from the ECB meeting, the Eurozone bank lending survey tomorrow is important in order to see how lending standards have moved from what are currently tight and restrictive levels. The Fed’s SLOOS equivalent is out next week and is also very important. These are key pillars in the recession argument and if they stay tight risks continue to build. A surprise big improvement will put a dent in the argument.

The BoJ will close out the busy week for central banks with a decision on Friday and will also release their quarterly Outlook Report. DB's Chief Japan economist previews the meeting here and sees some policy revision as a c.40% probability event, but continues to expect no change in monetary stance as his baseline. For the Outlook Report, he expects the BoJ to increase the inflation outlook for FY2023 but lower it for FY 2024, continuing to emphasize downside risks, but with no changes to the growth outlook.

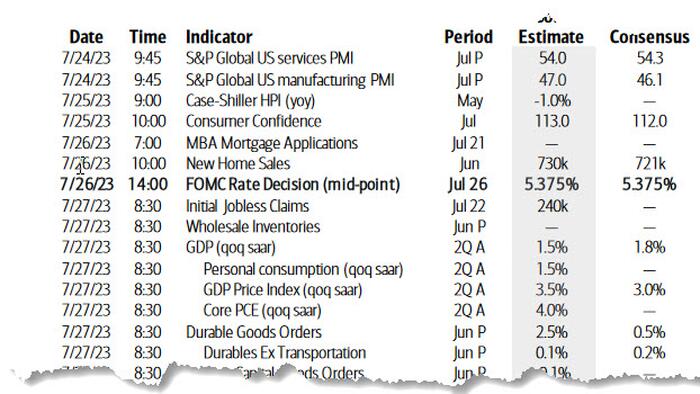

Turning to the week's economic indicators, several important gauges will be out in the US. This includes the preliminary Q2 GDP reading on Thursday as well as the employment cost index and personal income and spending on Friday along with the all important monthly core PCE. Other data in focus will include Conference Board's consumer confidence gauge (tomorrow), new home sales (Wednesday) and durable goods orders (Thursday).

Outside of the global flash PMIs today, a number of sentiment gauges will also be out in Europe, including the Ifo survey for Germany (tomorrow) and consumer confidence for France (Wednesday) and Germany (Thursday).

Germany and France publish preliminary CPI releases for July on Friday. Q2 GDP for France will be due that day as well. DB expects the headline gauge for the Eurozone to come in at 5.3% YoY (vs 5.5% YoY in June) and core at 5.4% (5.5%).

Corporate earnings releases will also compete for investors' attention with key big tech players, oil majors, semiconductor companies as well as some large European corporates, including those in healthcare and luxury, all reporting this week. The highlight will be big US tech, with Microsoft, Alphabet (tomorrow) and Meta (Wednesday). The three companies make up almost $5tn in market cap, or c.12% of S&P 500, and have enjoyed YTD gains ranging from around 36% for Alphabet to c 145% for Meta, helping propel the Nasdaq 100 to +41% YTD. Elsewhere in tech, Samsung, NXP semiconductors, Intel, Lam Research and SK Hynix will be among the companies reporting. Our US equity analysts preview the earnings season for semiconductors here, cautioning on the AI optimism.

Another notable group to release earnings will be the big oil firms. The list of companies reporting includes Exxon and Chevron on Friday in the US as well as Shell, TotalEnergies on Thursday and Eni on Friday in Europe. Elsewhere, Rio Tinto, Anglo American and Vale will be on investors' radars.

In terms of Consumer stocks, results are due from Coca-Cola, P&G, Mondelez and McDonald's, among others. Automakers releasing earnings include GM and Ford in the US and Porsche, Mercedes-Benz and Volkswagen in Europe. Otherwise, Raytheon, GE and Honeywell will be among notable industrials firms reporting.

Other European corporates reporting include healthcare firms AstraZeneca, Roche and Sanofi as well as a number of key European luxury firms such as LVMH tomorrow. Nestle and BASF will also report. The earnings and data highlights are in the day-by-day calendar at the end as usual. It’s certainly a busy week all round.

Courtesy of DB, here is a day-by-day calendar of events:

Monday July 24

Tuesday July 25

Wednesday July 26

Thursday July 27

Friday July 28

Finally, looking at just the US, Goldman notes that key economic data releases this week are the Q2 GDP report on Thursday and the core PCE and ECI reports on Friday. The July FOMC meeting is this week, with the release of the statement at 2:00 PM ET on Wednesday, followed by Chair Powell’s press conference at 2:30 PM.

Monday, July 24

Tuesday, July 25

Wednesday, July 26

Thursday, July 27

Friday, July 28

Source: DB, Goldman, BofA