As we start October, DB's Jim Reid asks whether we can power out of the gravitational pull of bad September seasonals. He notes that September 2023 was the 4th year in a row that the S&P 500 and the STOXX 600 were down for the month, as well as the 7th year in a row that Bloomberg’s global bond aggregate was down for the month. The damage in bonds has been more severe and more sustained than for equities and you can’t help wondering where the real damage is. The bottom line as the strategist puts it, is that "you can’t have this much value destruction in bonds without there being some stress somewhere. However, it’s near impossible to work out where exactly it might come to the surface."

One thing that is certain is that it will, just give it time.

The good news as we start the week and the new business month is that the US averted a shutdown just before the deadline on Saturday night which will keep the government running until November 17th. This gives negotiators more time to pass something more long standing. We will see if we’re in the same position in six weeks' time though.

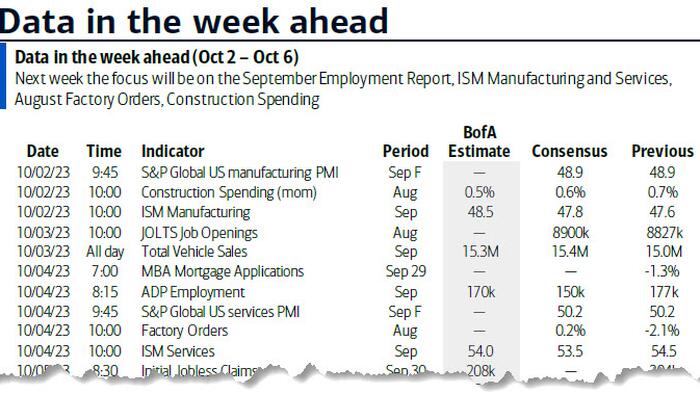

For now no shutdown means that US data will get published on time this week. The highlight is clearly Friday’s payrolls. Before that, the JOLTS (tomorrow) and ADP (Wednesday) data will give us some early clues. The former is a month behind but is obviously a key report to assess labour market tightness by looking at the quits rate, hirings and vacancies etc.

The highlights for the rest of the week are the US ISM and a Powell roundtable discussion today, an expected hold from the RBA tomorrow, US services PMI, Euro Zone retail sales, Euro Zone PPI and a Lagarde speech on Wednesday, French IP on Thursday with German factory orders on Friday. The full week ahead is at the end, including a bevy of central bank speakers, but we’ll quickly preview today’s ISM and Friday’s payrolls below.

Going back to the main events, DB's economists and the consensus are expecting +165k for headline payrolls (+187k previously) with the unemployment rate expected to dip back down a tenth to 3.7% after surprisingly increasing three tenths last month. A reminder that every headline payroll number has now been revised lower in 2023. In early summer we were on a run of 13 successive beats but some of that has now gone with revisions.

Today’s US manufacturing ISM (47.5 expected at DB vs. 47.6 last) and Wednesday's services ISM (54.1 vs. 54.5) are expected to be fairly stable. For the former our economists’ models suggest an uptick but the UAW strikes could offset that as perhaps foretold by a weak Chicago PMI last week. Note that it’s likely too early for this strike to impact payrolls but it could make a sizeable impact next month. For services watch for the employment index as this surprisingly soared 4 points to 54.7 last month.

Talking of such indices, the official China manufacturing PMI edged up to 50.2 (50.1 expected) over the weekend from 49.7 in August. Services also beat by a tenth to 51.7 from 51.0 in August. The private Caixin equivalents were at 50.6 and 50.2 respectively, below the 51.2 and 52.0 expected. So a mixed set of data as China starts a holiday week.

Courtesy of DB, here is a day-by-day calendar of events

Monday October 2

Tuesday October 3

Wednesday October 4

Thursday October 5

Friday October 6

Turning to just the US, Goldman writes that the key economic data releases this week are JOLTS job openings on Tuesday, the ISM services report on Wednesday, and the employment report on Friday. There are many speaking engagements from Fed officials this week, including Chair Powell, governors Bowman and Waller, Vice Chair for Supervision Barr, and presidents Harker, Williams, Mester, Bostic, Goolsbee, and Daly.

Monday, October 2

Tuesday, October 3

Wednesday, October 4

Thursday, October 5

Friday, October 6

Source: DB, Goldman. BofA