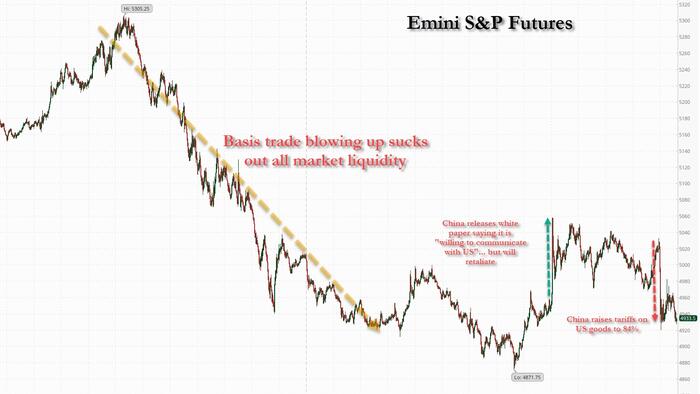

The rollercoaster goes on as stock futures continue to swing wildly, and now we have the extra kicker of the $2 trillion basis trade blowing up and sending bond yields soaring in the US and across most developed economies just as stocks tumble, leading to a complete wipe out of all 60/40 "balanced" portfolios. US futures had slumped as much as 3% overnight amid the ongoing collapse of the basis trade, which we first profiled here, only to reverse and turn briefly green just after 3am ET after China released a White Paper on US trade in which it hinted that it was "willing to communicate with the US" but that initial bounce quickly faded after China also warned it would retaliate... and then it did just that after 7am ET, when Beijing announced it would match Trump's latest and raise tariffs on US goods to 84%; this quickly sent futures back near sesion lows and down 2%. Pre-market, Mag 7 names were mixed (Tesla +0.39%, Nvidia +0.22%, Apple +1.1%, Meta +1%, Amazon +1%, Alphabet -0.9%, Microsoft -0.8%), while healthcare stocks were lower as pharma tariffs are earmarked to be released soon. Meanwhile, as we described first late last night, forced sales resulting from the unwind of the basis trade have slammed the Treasury market, where yields surged over the last few sessions and 2Y to 30Y yields are higher again today. At one point the 10Y was as high as 4.50%; this morning JPM asks a question: "If trade imbalances are zeroed out, do foreign countries need to hold Treasuries?" USD is weaker and commodities are mixed with Base Metals/ Energy lower, goal soaring higher, and Ags mixed. Fed Minutes are released this afternoon with CP| tomorrow.

{kind=link}

In premarket trading, Mag 7 names were mixed (Tesla +0.39%, Nvidia +0.22%, Apple +1.1%, Meta +1%, Amazon +1%, Alphabet -0.9%, Microsoft -0.8%), while drugmaker stocks slide after Trump said the US is planning to announce “a major tariff” on the sector soon: (Pfizer -4.1%, Merck -3.4%, Bristol-Myers Squibb -3.9%, Biogen -2.0%, Eli Lilly & Co -3.3%, Amgen -3.7%, Moderna -2.5%, Johnson & Johnson -3.4%). US-listed Chinese stocks pare gains from earlier in the premarket session or fall as China retaliates with an 84% tariff on US goods (Alibaba +3.1%, Nio +0.32%, Baidu +0.18%, PDD -1.6%, JD.com +2.9%, NetEase +0.40%, Trip.com +2.5%, Li Auto +1.0%, KE Holdings +2.2%, Bilibili +4.2%). Here are some other notable movers:

While China's escalation was notable, if expected, the biggest news overnight was the collapse of the basis trade, which we first correctly predicted last week and described overnight; this is sending yields soaring amid forced liquidations, even as stocks continue to slide.

“We’re well into an escalation phase in the trade war and investors have just nothing to hold onto at the moment,” said Alexandre Baradez, chief market analyst at IG Markets Ltd. “What’s clear now is that the US bond market is no longer a safe haven for investors, but on the contrary is piling pressure on stock markets.”

Meanwhile, shares in large US and European drugmakers fell after Trump said the US was planning to announce “a major tariff on pharmaceuticals” soon. Pfizer Inc., Eli Lilly & Co. and Merck slid more than 3% in US premarket trading.

The worsening trade conflict, with Trump raising levies on China to 104% at midnight, has been condemned by investors including Bill Ackman and prompted economists at JPMorgan and Goldman to raise the probability of a US recession. That would complicate the Federal Reserve’s policy response if it has to contend with an inflation spike brought on by the tariffs.

Investors were gripped by concerns that something may break in the financial plumbing as volatility and stress build across markets. Ray Dalio, the billionaire founder of Bridgewater Associates, warned about a “once-in-a-lifetime” breakdown occurring in monetary, political and geopolitical orders.

“We’re reaching a new stage in the selloff with now serious concerns that the high volatility could trigger market accidents and possibly something systemic,” said Alexandre Hezez, chief investment officer at Group Richelieu in Paris. “If the Fed is forced to intervene and cut interest rates despite Trump’s inflationary policies, then 10-year yields will jump even further.”

Europe's Stoxx 600 drops 3%, with all sectors in the red. Health care, energy, and telecoms lead losses. UK and German yield curves steepen as two-year yields drop, while long-end rates climb. Here are the biggest movers Wednesday:

Earlier in the session, Asian stocks dropped as tariffs implemented by President Donald Trump took effect, with total levies on China climbing to 104%. The MSCI Asia Pacific Index fell 1.4%, with TSMC, Hitachi and Mitsubishi among the biggest drags. Taiwan’s benchmarks tumbled more than 5%, while key gauges slid more than 3% in Japan. Shares in Korea slumped into a bear market territory, while shares in Hong Kong and China advanced thanks to continued buying by China's plunge protection team. Markets “probably will continue to see some wild gyrations this week, and longer as markets work through this tariffs episode,” said Kok Hoong Wong, head of institutional equities sales trading at Maybank Securities. Potential responses from Europe and elsewhere will be among key points to watch.

The exodus spread to other markets. The UK’s borrowing costs surged to the highest since 1998, and Japanese 40-year bond yields struck a record high. US treasuries also held losses, extending past week’s steep selloff, with some paring after China raised tariffs on US goods to 84%, triggering a drop in stock futures. Intermediate and long-end yields are higher on the day by as much as 10bp, front-end by about 4bp. US yield curve has steepened further, though spreads are off session highs, with 2s10s wider by about 4bp, 5s30s by about 1bp; 10-year yield around 4.37% is 8bp higher on the day, with bunds outperforming by around 9bp in the sector, gilts by ~1bp.

UK 30-year yields earlier hit their highest since 1998, as contagion from the selloff in US 30-year bonds spread. Swap spreads - which is where the collapse of the basis trade can be seen clearest - likewise extended past week’s violent narrowing move, with long-end tenor dropping as low as -100bp. US session includes $39 billion 10-year note auction at 1pm New York time. Treasury auction cycle continues with $39 billion 10-year note reopening, following soft demand for Tuesday’s 3-year note sale, which tailed by 2.4bp tail and had above-average dealer allocation. Cycle concludes Thursday with $22 billion 30-year

In FX, the Bloomberg Dollar Spot Index falls 0.5% while the Aussie dollar climbs 1% versus the greenback, topping G-10 FX.

In commodities, spot gold surges ~$75 to around $3,056/oz. Oil prices decline, with Brent falling close to 4% to just above $60 a barrel.

Looking at today's calendar, all eyes will be on the trade war and swap spreads US economic calendar includes February wholesale inventories at 10am; Fed speaker slate includes Barkin at 11am at Economic Club of Washington DC; minutes of FOMC’s March meeting will be released at 2pm

Market Snapshot

Top Overnight news

Trade/Tariffs: US

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower following the dead cat bounce on Wall St and as reciprocal tariffs took effect overnight including a total 104% tariff on China. ASX 200 was dragged lower by underperformance in health care and miners with the former pressured after US President Trump stated that he will be announcing tariffs on pharmaceuticals soon. Nikkei 225 spearheaded the declines in Asia and fell beneath the USD 32,000 level amid currency strength and ongoing tariff woes with a report noting that tariffs could potentially reduce Japanese companies' earnings by up to 10%. Hang Seng and Shanghai Comp were mixed as the Hong Kong benchmark conformed to the losses in the region, while the mainland traded indecisively and was somewhat cushioned following recent stabilisation measures and expected policy support.

Top Asian News

European bourses (STOXX 600 -3%) are entirely in the red, but off worst levels after sentiment improved around the European cash open which coincided with commentary from China’s Foreign Ministry, which avoided announcing any fresh retaliation to Trump's latest tariffs. European sectors are in negative territory, but display a more improved picture than opening levels. Healthcare is by far the clear laggard as markets digest the latest commentary from US President Trump who said that he will be announcing tariffs on pharmaceuticals soon. Energy is also amongst the underperformers, as underlying oil prices remain pressured.

Top European News

FX

Fixed Income

Crude

Geopolitics

US Event calendar

Central Bank speakers

DB's Jim Reid concludes the overnight wrap

The market turmoil has shown no sign of letting up over the last 24 hours, with the S&P 500 (-1.57%) edging increasingly close to bear market territory, having now shed -18.9% since its peak in mid-February. Moreover, futures are still pointing towards further losses today, with those on the index down another -2.53%, which if realised would take us over the bear market line. Perhaps even more alarmingly, US Treasury markets are also experiencing an incredibly aggressive selloff as we go to press, adding to the evidence that they’re losing their traditional haven status. That’s been particularly evident at the long end of the curve, with the 30yr yield up another +19.3bps this morning to 4.96%, having already risen by +35.6bps over the previous two sessions (the fastest move higher since March 2020). So there’s no sign yet that the market is managing to successfully find a bottom, and it feels like no asset class has been spared as investors continue to price in a growing probability of a US recession.

It had been a very different story at the open, as hopes for negotiated deals initially saw the S&P 500 surge by more than +4%. However, several triggers drove a sharp turn lower in market sentiment as the day went on. First, we had confirmation from US officials that the additional 50% tariff that Trump threatened China with on Monday would be imposed, dashing any remaining hopes for a last minute extension before the deadline. These reciprocal tariffs have now gone into effect as of 5am London time, meaning that the total China tariff now stands at 104%, with overall US tariffs now at their highest level since the early 20th century. In the meantime, there was little let up in Trump’s tone on tariffs last night, with the President saying that “we’re going to be announcing very shortly a major tariff on pharmaceuticals”.

Second, yesterday saw a weak 3yr Treasury auction, which exacerbated fears about how much demand there still was for the asset. They were issued 2.4bps above the pre-sale yield as the bid-to-cover ratio fell to its lowest in six months. So that helped contribute to a huge selloff among longer-dated bonds, and this morning the 10yr yield is up another +16.7bps to 4.46%. Given the scale of the rout, that’s raising questions about whether the Federal Reserve might need to respond to stabilise market conditions, and we can even see from fed funds futures that markets are pricing a growing probability of an emergency cut, just as we saw during the Covid turmoil and the height of the GFC in 2008.

Third, another story in the background has been a sharp weakening in the offshore yuan, which fell to its lowest level in history against the dollar, raising concerns that China could resort to competitive currency devaluation in response to US tariffs. So it’s exacerbating fears that the US and China could end up in an escalatory spiral that opens up further downside risks. That saw it decline to 7.43 per dollar, though it has since recovered to 7.38 overnight. Interestingly, equity indices in mainland China are the one positive performer overnight, with the CSI 300 (+0.32%) and the Shanghai Comp (+0.24%) both rising slightly. Elsewhere however, the overnight performance has been dire, with the Nikkei (-4.11%) slumping back after its rally the previous day, along with the KOSPI (-1.76%), the S&P/ASX 200 (-1.83%). Futures are all pointing that way as well, with those on the German DAX slumping -3.88%, whilst those on the S&P 500 are down -2.53%.

Taking a historic view, the -18.9% decline in the S&P 500 means it’s now becoming one of the bigger selloffs of recent history. Indeed, yesterday it surpassed the 2015-16 decline (-18.3%), which was driven by fears of a hard landing in China, a US growth slowdown, and the start of Fed hikes. The next threshold in recent times would be the late-2018 selloff, when the index fell -19.8% (also amidst Fed rate hikes and a growth slowdown, alongside trade tensions). And currently, futures are suggesting the index would be -21.0% lower, meaning it would overtake that selloff if realised. However, there’s still further to go before we get to the scale of the 2022 bear market (-25.4%), back when the Fed hiked aggressively to combat inflation and recession fears mounted. And we’re even further from the biggest fall of the last decade, which was the Covid shock, when the index fell -33.4% in little over a month.

In terms of the market reaction yesterday, there was little respite wherever you turned. The S&P 500 has now fallen -12.1% since the reciprocal tariff announcement, making it the biggest 4-day decline since March 2020, when the index saw a -17.2% drop as the world moved into lockdowns. It also saw a trading range above 5% for the fourth day running. In another sign of stress, the VIX index of volatility continued to mount, up +5.35pts to 52.33pts. Bear in mind the only other times it’s closed that high were during the Covid turmoil and the height of the GFC. Credit also remained under pressure, with US HY spreads widening another +4bps to 453bps, the highest they’ve been since June 2023. Otherwise, the selloff meant oil prices continued to plummet as well, with Brent crude (-2.16%) falling to $62.82/bbl yesterday, and this morning it’s down another -4.09% lower this morning at $60.25, its lowest level in four years.

It feels like ancient history now, but at the US open yesterday, there had actually been a much more positive narrative that helped the S&P 500 surge more than +4%. That was in part thanks to various comments suggesting that trade deals might be reached with various other countries. For instance, President Trump himself posted that he had he’d spoken with the Acting President of South Korea, and that “we have the confines and probability of a great DEAL for both countries.” On top of that, he said “We are likewise dealing with many other countries, all of whom want to make a deal with the United States.” Similarly, Treasury Secretary Bessent said on CNBC that if US trading partners “come to the table with solid proposals, I think we can end up with some good deals”. So that further added to hopes that Trump would negotiate the tariffs down over time.

Indeed, before we had that selloff later in the US, European assets had seen a much better performance yesterday, as markets closed before the evening selloff. So by the close, the STOXX 600 (+2.72%) had put in a strong rebound, posting its best daily performance since November 2022. Likewise for rates, the moves in the 10yr were comparatively steady, with those on 10yr bunds (+1.8bps) only seeing a modest increase, whilst those on 10yr OATs (-0.9bps) and BTPs (-0.9bps) fell back slightly. At the same time, 10yr gilts (-1.3bps) also saw a decline in yields, but the 30yr yield (+2.7bps) continued to move higher, closing at 5.35%.

Finally on the data side, we also got the NFIB’s small business optimism index for March yesterday, which contained growing evidence that the tariff impact was having an effect. It was conducted before the reciprocal tariff announcement, but concern was already mounting given the moves on Canada, Mexico and China, and we’ve seen other confidence surveys take a hit as a result. This one was no different, and the main index fell by more than expected to 97.4 (vs. 99.0 expected), in what also marked the biggest monthly decline since June 2022, back when inflation was still well above target and the Fed were hiking rates aggressively. Notably, there was also a sharp dip in the proportion saying they expected the economy to improve, falling back to a net +21%, having been at +37% in February. Indeed, it was the sharpest monthly drop since December 2020.

To the day ahead now, and the main things to look out for will be on the central bank side, including the minutes from the FOMC’s March meeting. Otherwise, we’ll hear from BoJ Governor Ueda, the ECB’s Knot, Villeroy and Cipollone, and the Fed’s Barkin.