US equity futures are higher as futures pointed to a rebound from yesterday’s selloff, while the yen weakened on a BBG report that the the Bank of Japan won’t make any changes to its yield curve control program. As of 7:45am ET, S&P futures were 0.2% higher while Nasdaq futures rebounded 0.4% from yesterday's 2.3% rout. Netflix and Tesla climbed in pre-market trading after leading the Nasdaq to sharp losses on Thursday on the back of disappointing results. The Bloomberg Dollar Spot Index traded near the day’s highs, pressuring most Group-of-10 currencies, with the yen suffering the biggest declines after Bloomberg reported that Bank of Japan officials see little urgent need to address the side effects of its yield curve control program. Treasury yields were little changed, mirroring lackluster trading in European and UK bond markets. Brent crude rose more than 1%, while gold fell and Bitcoin gained 0.2%. The Nasdaq rebalance will take effect after close today. Headlines remain quiet this morning; next week, we will receive key MegaCap Tech earnings, starting with GOOGL and MSFT on Tuesday (7/25), and the July FOMC on Wednesday.

In premarket trading, American Express fell almost 3% after the company reported discount revenue for the second quarter that missed the average analyst estimate. Tesla led electric-vehicle stocks higher in US premarket trading after weighing on the sector on Thursday. The stock had slumped after the world’s most valuable carmaker warned of more hits to its already-shrinking profitability. Digital World Acquisition Corp, the SPAC working to bring Donald Trump’s media venture public, soared 21% in premarket trading on Friday after the SEC said it settled fraud charges against the SPAC. Here are some other notable premarket movers:

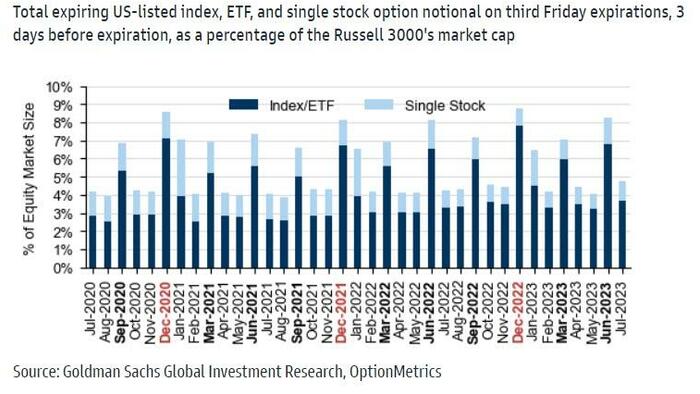

Trading on Friday will be affected by a flood of expiring options before an out-of-cycle rebalancing in the Nasdaq 100. The index shuffle, which takes effect on Monday, is designed to reduce the dominance of megacaps and boost the presence of smaller members. The tech-heavy index’s rejig coincides with the monthly options expiration - which at $2.4 trillion is a record for the month of July (see our preview here)- at a time when traders are anxiously waiting for corporate earnings and next week’s Federal Reserve policy meeting for clues on the market’s outlook.

Stocks slipped Thursday for the first time this week as fresh signs of labor-market resiliency bolstered the case for at least another Fed hike this year. Underscoring the risk-off mood, investors withdrew $2.1 billion from equity funds in the week to July 19, while adding $7.5 billion to money markets and $1.4 billion to bond funds, according to BofA's Michael Hartnett.

The main focus continues to be whether the rally in a handful of megacap stocks and hype over artificial intelligence has staying power. The S&P 500 has already surpassed most estimates for where it would end the year, confounding strategists convinced that 2023 would be another bad year for markets heading into recession.

“So where we are right now, we are resting after the massive move over the course of many weeks,” Ken Mahoney, CEO of Mahoney Asset Management, wrote in a note. “A lot of stocks were creating and still are creating bases to break out higher from. No one could believe their eyes after being so conditioned to 2022’s nasty selling conditions when this market gained steam again.”

European stocks were mixed, trading between gains and losses with the German DAX underperforming as SAP shares slump after cloud sales missed estimates. Here are the most notable European stock moves:

Earlier in the session, Asian stocks dropped, as tech stocks led losses following TSMC’s guidance cut while benchmarks in Hong Kong climbed. The MSCI Asia Pacific Index slumped 1.5% mainly because of the sharp drop in Indian stocks. TSMC, Tokyo Electron and other chip stocks were the biggest drags on the gauge after TSMC cut its annual outlook for revenue and delayed production at a planned facility in Arizona. The Hang Seng China Enterprises Index advanced as much as 1.4%, while other other Hang Seng gauges were also among the region’s notable outperformers. Their gains come after losses in the past several sessions amid disappointments over the second-quarter growth figures and underwhelming support pledges from Beijing. Investors said the valuations of Chinese equities remained cheap even as it may take time to see a comeback in investor confidence.

Japan's Nikkei 225 slumped at the open but was well off its lows amid currency swings and somewhat ambiguous CPI data which printed mostly in line with expectations but showed a slight acceleration for the headline and core inflation.

Key stock gauges in India snapped a six-day winning run to end as the worst performing market in the region on Friday due to a sell off in technology stocks. The S&P BSE Sensex fell 1.3% to 66,684.26 in Mumbai, while the NSE Nifty 50 Index declined 1.2% to 19,745.00. For the week, Sensex and Nifty climbed about 0.9% on continued net buying from foreign institutional investors amid optimism for earnings growth. Global funds net buying of India stocks have climbed to more than $15 billion since February. The MSCI India index ended with a 9.2% drop after a sudden decline in the index around 1:20 pm with index provider MSCI saying it is looking into the movement.

“We need to see evidence of economic data recovering,” Abhilash Narayan, senior investment strategist at Standard Chartered Wealth Management, said in an interview with Bloomberg TV. “But from a valuation perspective, Chinese equities are extremely cheap,” he said adding that there is “a fairly good likelihood” that they will outperform global peers over the next 12 months. The main Asian equity benchmark is set for about a 1% decline this week, its worst weekly performance this month. Investors are monitoring corporate earnings reports with many heavyweights in Asia scheduled to report their quarterly results next week.

In FX, the Bloomberg dollar index extended gains to a fourth day, its longest winning streak since May. The yen tumbled as much as 1.4% and led losses among Group-of-10 currencies after traders confirmed what we have been saying all along - that there is little chance for a hawkish surprise at the BOJ’s policy decision next week as Bloomberg reported that officials see little urgent need to address the side effects of its yield curve control at this point.

The currency traded at 141.81 against the dollar, its weakest level in almost three weeks, amid reduced odds for a hawkish surprise at the BOJ’s policy decision next Friday.

In rates, treasury yields edged lower as US trading day begins, led by longer-dated tenors. Narrow ranges during Asia session and European morning include 2.4bp for 10-year yield. On the week, yields are likewise mixed with the curve flatter, after swaps fully priced in a Fed rate hike on July 26 while auctions of 20-year bonds and 10-year TIPS drew strong demand. Yields remain within about 2bp of Thursday’s closing levels, 10- year around 3.84%, holding above 50-day average level breached this week for the first time since May; most other sovereign debt markets also little changed. Inverted 2s10s curve slightly flatter on the day at around -100bp; Thursday’s low -105bp was deepest inversion since July 6. Fed swaps continue to fully price in a 25bp rate hike on July 26 and about a third of an additional quarter-point hike this year.

The pound also jumped after UK retail sales topped estimates, although gains proved short lived with cable now negative. The Bloomberg Dollar Spot Index is up 0.3%. European stocks are little changed with the Stoxx 600 flat after a three-day rally.

Wall Street looks set for a higher open with S&P futures up 0.2% and Nasdaq 100 futures adding 0.4%. Gilts are in the red while bunds and Treasuries trade close to unchanged. Crude futures advance, with WTI rising 1.2% to trade near $76.60

In bitcoin, US House Republicans introduced a new digital assets oversight bill that aims to establish a regulatory framework to protect crypto investors, according to CoinDesk. FTX sues Sam Bankman-Fried and other former executives to recoup hundreds of millions of dollars of alleged fraudulent transfers, according to Reuters.

In commodities,

Wheat fell about 3% as Ukraine made preparations to continue a grain-export deal, which Russia exited this week. The grain is still poised for a weekly gain of 7%, after prices surged on threats to ships arriving at Black Sea ports. The rise in prices could again stoke food costs and feed inflation.

Looking to the day ahead, it’s a fairly quiet one on the calendar with nothing on the US docket. Global data releases include UK retail sales for June, which came in handily above expectations, while earnings releases include American Express which missed expectations.

Market Snapshot

Top Overnight News from Bloomberg

A more detailed look at global markets courtesy of newsqquawk

APAC stocks were mixed as further support efforts from China partially offset the headwinds from Wall St where the Nasdaq 100 suffered its second-worst day of the year on tech disappointment and amid a rising yield environment. ASX 200 was subdued amid losses in tech, financials and the mining-related sectors, albeit with downside limited amid the lack of catalysts from Australia. Nikkei 225 slumped at the open but was well off its lows amid currency swings and somewhat ambiguous CPI data which printed mostly in line with expectations but showed a slight acceleration for the headline and core inflation. Hang Seng and Shanghai Comp were underpinned by further supportive efforts from China in which the NDRC released policies to boost electronics products consumption and measures to promote automobile consumption.

Top Asian News

European bourses are relatively steady after mixed APAC performance as Chinese support offset the subdued handover, Euro Stoxx 50 -0.1%; in Europe, Tech lags with SAP -3.9%. Sectors are somewhat mixed with Energy seeing upside on benchmark pricing, though off best as the USD picks up, while Tech and the DAX 40 -0.5% lag after SAP missed on top & bottom. Stateside, futures are little changed amid a sparse US-specific docket ahead, ES +0.1%; NQ +0.3% is the incremental outperformer after Thursday's marked pressure and as the dovish-BoJ reports lend support via lower yields.

Top European News

FX

Fixed Income

Commodities

Geopolitics

US Event Calendar

DB's Jim Reid concludes the overnight wrap

After a pretty strong last couple of weeks for bonds and equities, both sold off yesterday in the US, with tech having one of the worst days of the year. Ironically, outside of disappointing tech earnings, the main catalyst was actually some positive US data, which shifted the debate back towards next week not necessarily being the last Fed hike in the cycle.

Indeed, more hawkish expectations meant that the 2yr real yield hit a post-GFC high intra-day, though it was breakevens that drove the rates sell off at the end of the day. The rates environment was a setback for equities, while weak tech earnings releases weighed even more, with the NASDAQ falling -2.05% in its biggest post-SVB decline and the 3rd worst day of the year.

In terms of the specific data releases, the most important were the weekly US initial jobless claims, which fell to 228k (vs. 240k expected) over the week ending July 15. That’s the lowest claims number we’ve had in a couple of months, and there are growing signs that this is a trend, with the 4-week moving average down for a third week running to 237.5k. It’s true that the continuing claims were above expectations at 1.754m (vs. 1.722m expected), but that was for the previous week ending July 8, and the broader trend downwards is also still evident from the chart. As well as the jobless claims, the Philadelphia Fed released their manufacturing business outlook survey, with the headline index up slightly to -13.5 (vs. -10.0 expected). But the much better news was on the expectations side, with the headline index for 6 months from now up to a 23-month high of 29.1.

With those more positive releases in hand, investors moved to price in a growing chance of further hikes over the months ahead. For instance, futures raised the chances of a second further hike from the Fed after next week to 35%, having been at 30% the previous day. They also dialled back the chances of rate cuts in 2024, with the rate priced in for December up +10.4bps on the day to 4.03%. In Europe it was much the same story, albeit to a lesser extent, with pricing for a second ECB hike after next week up from 87% to 94%.

All that led to a significant selloff among sovereign bonds, with yields on 10yr Treasuries up +10.3bps on the day to 3.85%. That’s their biggest increase in three weeks, and this was echoed across the curve, with the 2yr yield up +7.4bps to 4.84%. As mentioned at the top, there was a shift in the drivers of higher rates through the course of the day. The 2yr real yield hit a post-GFC high intra-day, but breakevens drove most of increase by the close with 10yr breakevens (+8.6bps) seeing their sharpest daily rise since January.

Europe got some positive, albeit backward looking, economic news as well yesterday, as the latest data revisions showed that the Euro Area avoided a technical recession over the winter. That’s because growth in Q1 was revised up to 0.0% (vs. -0.1% previously), so the latest data now only shows one quarterly contraction in Q4, rather than the two consecutive contractions that are often used to define a recession. Alongside the US data, that supported a fresh rise in yields there too, with those on 10yr bunds (+4.6bps), OATs (+5.0bps) and BTPs (+2.9bps) all moving higher.

This put a dent in US equities, with the S&P 500 (-0.68%) seeing its biggest decline in two weeks. That said, more than 50% of the S&P 500 actually posted gains on the day with the decline driven by tech stocks. Tesla (-9.74%) and Netflix (-8.41%) both lost significant ground following their earnings after the previous day’s close. This weakness among tech stocks meant that the NASDAQ (-2.05%) suffered its worst day in four months, whilst the FANG+ index (-4.60%) of megacap tech stocks had its worst day of 2023 so far. In other negative news on the tech front, leading chipmaker TSMC cut its 2023 outlook and signaled a delay on a new planned production facility in Arizona. TSMC shares are trading more than -3% lower in Asia this morning. Finally, the underperformance of tech megacaps may have been exacerbated by a special rebalancing of the NASDAQ 100 index, which will be effective as of next Monday (24 July) and will see a decline in the index weights of the tech megacaps.

On the other hand, with utilities, energy and industrials outperforming, the Dow Jones (+0.47%) advanced for a 9th consecutive session for the first time since 2017. The European bourses also fared much better, with the STOXX 600 up +0.42% to a one-month high.

In the geopolitical sphere, Ukraine said that ships heading to Russian ports may be military targets following the collapse of the Black Sea grain deal, which comes in response to Russia announcing a similar move regarding ships heading to Ukraine. Wheat prices initially spiked higher following the news, but they pared back their gains and ended the session -0.10% lower after a run of 5 consecutive gains. They are +17% up from their recent lows on 12 July.

Asian equity markets are mixed this morning with the Hang Seng (+0.80%) leading gains while the CSI (+0.24%) and the Shanghai Composite (+0.08%) edging higher after the Chinese government announced detailed measures to support the private sector. Elsewhere, the Nikkei (-0.22%) is lower with the KOSPI (-0.08%) swinging between gains and losses. S&P 500 (+0.12%) and NASDAQ 100 (+0.11%) futures have seen a small rebound.

Early morning data showed that Japan’s consumer inflation climbed by +3.3% y/y in June (v/s +3.2% expected), and slightly higher than May’s +3.2% increase while the core consumer prices rose +3.3% y/y in June, in line with market expectations and against the prior month’s gain of +3.2%. Core core was in-line at +4.2% y/y, down a tenth from last month, the first decrease in the y/y rate since January and likely marks the start of a trend lower. The pace of the decline will determine the BoJ's policy over that period though. Remember we have an important BoJ meeting next week with some whispers of policy change although the market will be once bitten twice shy on this.

In UK by-elections, the Conservative government suffered a double by-election defeat after Selby and Ainsty (considered as a safe seat) voted against the government giving the Labour its largest swing since 1997 and its biggest ever reversal of a numeric majority in a by-election in history. The Government surprisingly held ex-PM Boris Johnson's seat in Uxbridge London, as an unpopular scheme by the Labour London mayor on expanding the ultra low emissions zone in the capital, put off voters.

Before we look at the day ahead a quick wrap of yesterday’s other data. US existing home sales for June fell to an annualised rate of 4.16m (vs. 4.20m expected), which is their lowest level in 5 months. Separately, the Conference Board’s leading index for June posted a -0.7% decline (vs. -0.6% expected), marking its 15th consecutive monthly decline. Finally in Europe, German PPI inflation fell to just +0.1% in June, which is its lowest level since November 2020.

To the day ahead now, and it’s a fairly quiet one on the calendar. Data releases include UK and Canadian retail sales for June, whilst earnings releases include American Express.