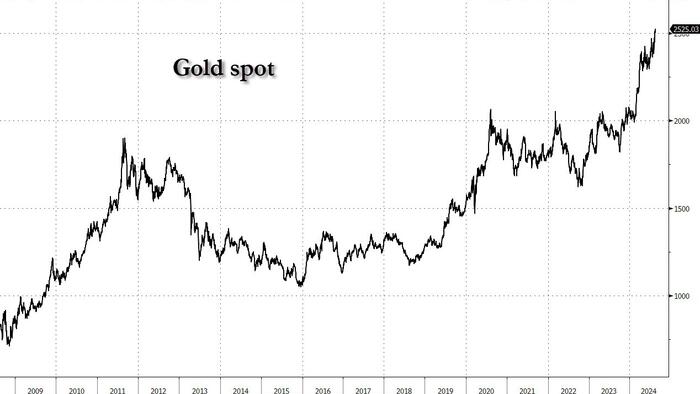

US equity futures are flat after another narrow overnight range, following another euphoric session on Wall Street amid bets the Fed chair Powell will signal it’s ready to start cutting interest rates as soon as this Friday's Jackson Hole symposium. As of 7:30am ET, S&P futures were up 0.1% to 5,634 while Nasdaq futures also gained 0.1%. MSCI’s all-country stock index headed for a ninth day of increases, its longest winning streak since December. Oil halted its latest rout, treasury 10-year yields held steady around 3.87%, the Bloomberg dollar index was unchanged after sliding to the lowest since March, while gold exploded to a new record high, trading at $2525. It is a quiet session with just the Philly Fed non-mfg activity index on deck.

In premarket trading, home improvement retailer Lowe's cut its sales and earnings forecast, blaming a frozen housing market. Hawaiian Holdings rose 10% after the US Justice Department decided against challenging its proposed tie-up with Alaska Air. Meanwhile, the European Union said it plans to introduce a 9% tariff on Teslas imported from China. Here are other notable premarket movers:

On the corporate front, Alimentation Couche-Tard Inc.’s preliminary proposal to buy 7-Eleven owner Seven & i Holdings Co. could be worth more than ¥5.63 trillion ($38.4 billion), based on the Japanese company’s market value after news of the potential deal was disclosed. Edgar Bronfman Jr. submitted a $4.3 billion bid to take control of Paramount Global and quash an existing offer from Skydance Media, Bloomberg reported.

Traders are taking a break after Monday’s session in the US lifted the S&P 500 for an eighth straight day. Stock volumes have been trending lower with investors reluctant to place big bets before central bankers gather for the Fed’s Jackson Hole economic symposium this week.

“What we’ve seen happen is a swath of recent data, which has eased fears about slowing US growth without stoking fears of re-accelerating inflation,” said Kyle Rodda, a senior market analyst at Capital.Com Inc.

With stocks relatively flat, attention has turned now to gold where the precious metal has broken out from its range and is hitting new record highs on an almost daily basis ahead of the coming dollar debasement about to be unleash by the Kam-unist regime of Kamala Harris who plans on "fighting" food inflation with price control. Gold has gained more than 20% this year, in part driven by the view that the Fed’s pivot toward cutting rates was nearing. Banks including UBS and ANZ say that there’s scope for further gains too, not just on the Fed’s policy but on central bank buying and demand for portfolio hedges.

{kind=link}

In Europe, technology and travel shares outperformed, keeping the Stoxx 600 within a whisker of recouping August’s losses as investors bet that interest rates in the US will ultimately come down. Technology is the strongest performing sector, with energy the biggest laggard as oil stocks fall on easing supply risks from a potential Gaza cease-fire. Here are some of the biggest European movers on Tuesday:

The recent turmoil in financial markets has left strategists unfazed about the outlook for European stocks. The benchmark gauge is seen ending the year at 535 points — about 4.6% above Friday’s close, according to the median estimate in a Bloomberg survey of 16 strategists. Still, increasing risks to the region’s growth outlook have reinforced the case for a policy adjustment when the European Central Bank meets next month, Governing Council member Olli Rehn said. Markets are pricing in at least two more rate reductions this year.

Asian stocks gained for a third day, helped by advances in Japan and South Korea amid optimism over Fed rate cuts. The MSCI Asia Pacific Index rose as much as 0.7%, with SK Hynix, Keyence and Samsung Electronics the biggest contributors to the advance. Key gauges in Japan climbed as the yen’s rally against the dollar stalled, supporting exporters such as tech companies and automakers. South Korean and Thai equities also gained.

In FX, the Bloomberg Dollar Spot Index is also little changed, trading near a 6 month low. The kiwi dollar tops the G-10 FX leader board, rising 0.4% against the greenback. The Swedish krona rises 0.3% even after the Riksbank cut interest rates and sketched out more easing than its previous guidance.

In rates, treasuries are steady, with US 10-year yields at 3.87%. The curve is steeper, unwinding much of Monday’s flattening move in 2s10s and 5s30s spreads. Corporate new-issue calendar may dominate the session, with Kroger expected to bring one of this year’s largest deals.

In commodities, WTI fell 0.6% to $73.95 after the US said Israel accepted a cease-fire proposal in Gaza, which however has zero chance of being accepted by Hamas. Copper steadied after a recent rebound and gold jumped by $18 to a record $2,525 an ounce on expectations that the Fed is poised to cut interest rates. Bitcoin gained 2%.

It's a quiet day: on the US economic calendar we only get the August Philadelphia Fed non-manufacturing activity at 8:30am. Fed speaker slate includes Bostic (1:35pm) and Barr (2:45pm)

Market Snapshot

Top Overnight News

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed and only partially took impetus from the tech-led gains stateside amid a lack of major macro drivers. ASX 200 edged mild gains with stock news in Australia dominated by earnings releases, while the RBA Minutes noted it is possible the cash rate would have to stay steady for an extended period and members agreed a rate cut in the short term was unlikely. Nikkei 225 outperformed and reclaimed the 38,000 level despite the absence of notable catalysts. Hang Seng and Shanghai Comp. declined amid lingering economic concerns, while China also maintained its Loan Prime Rates which was widely expected after last month's bout of cuts to key funding rates.

Top Asian news

European bourses, Stoxx 600 (+0.1%) are mostly, but modestly firmer (ex-FTSE 100), continuing the strength seen on Wall St in the prior session. FTSE 100 (-0.6%) is the worst performing index in Europe, weighed on by losses in Energy names amid the broader weakness in underlying oil prices; Shell (-1.8%), BP (-1.6%). European sectors are mixed; Tech takes the top spot, continuing the strength seen in the US on Monday. Travel & Leisure is also one of the better performers, benefiting from the recent drop in oil prices – as such, Energy is found at the foot of the pile. US Equity Futures (ES U/C, NQ U/C, RTY U/C) are flat, taking a breather following the significant strength seen in the prior session.

Top European news

FX

Fixed Income

Commodities

Geopolitics - Middle East

Geopolitics - Ukraine

US Event Calendar

Central Bank Speakers