A document released by the Federal Deposit Insurance Corp (or FDIC) which the agency said it mistakenly released unredacted in response to a Bloomberg News Freedom of Information Act request, has provided the most detailed glimpses yet into biggest Silicon Valley Bank customers who were bailed out when the Biden administration decided to backstop all the bank's deposits.

As a reminder, when regulators stepped in to backstop all of Silicon Valley Bank’s deposits back in March, they saved thousands of small tech startups to prevent what many (especially those whose money was tiled up with SVB) said would have been a catastrophic blow to a tech sector that relied heavily on the lender.

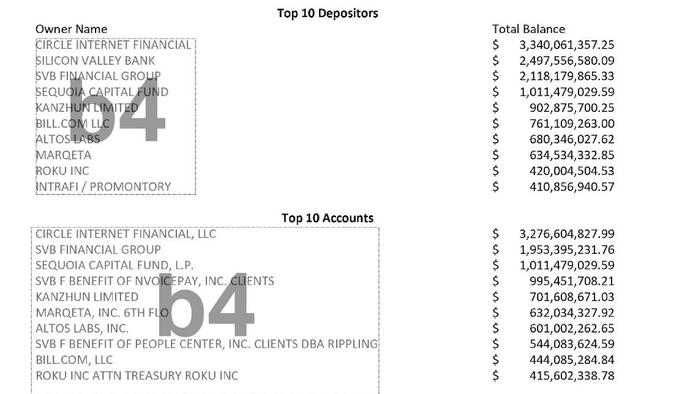

But the stunning decision to guarantee all accounts above the $250,000 federal deposit insurance limit helped bigger companies that were in no real danger. Among them was Sequoia Capital, the world’s most prominent venture-capital firm, which ended up recovering the $1 billion it had with the lender courtesy of taxpayers. Another was Kanzhun Ltd., a Beijing-based tech company that runs mobile recruiting app Boss Zhipin, which received a backstop for more than $900 million.

While the incompetent buffoons at the FDIC - which has been selling off pieces of the bank since its failure and which absurdly ended up giving JPMorgan a $50 billion loan in Jamie Dimon's taxpayer-funded rescue of First Republic Bank...

![]()

... asked that Bloomberg destroy and not share the depositor list, saying the agency intended to “partially” withhold some details from the document “because it included confidential commercial or financial information,” according to a letter from an attorney for the regulator. The agency subsequently declined to comment on the substance of the information in the document.

Bloomberg, however, refused to comply. The list - whose contents were largely known already except for a handful of names - mistakenly sent by the FDIC is below:

Back in March, when regional banks were falling like dominoes amid a cascading bank run targeting smaller US banks, regulators decided to declare a “systemic risk exception” and make all depositors at Silicon Valley Bank whole after a white-knuckled weekend in which tech founders digested SVB’s collapse on Friday, March 10 and were begging to be rescued.

Joe Biden described the solution as one that “protects American workers and small businesses, and keeps our financial system safe.”

Treasury Secretary Janet Yellen cast the government’s response - including backstopping all depositors - as necessary.

“American households depend on banks to finance their homes, invest in an education, and otherwise improve their standards of living. Businesses borrow from these institutions to start new companies and expand existing ones,” she said at an industry conference the following week before discussing the intervention.

In the end, US taxpayers ended up bailing out such VC titans as Sequoia; it's why the decisions that government agencies, including the FDIC, made in a frantic few days after SVB failed were immediately controversial.

Critics said that making all depositors whole at the lender and Signature Bank, which failed March 12, created a moral hazard. A fierce debate is also raging over whether the insurance limit needs to be raised for all businesses.

Former Vice President Mike Pence argued that backstopping all depositors amounted to a bailout - which of course it was - even though the Biden administration has forcefully pushed back against such a description. Pence blasted the government’s decision to insure all deposits, in part, because the move would cover Chinese companies that did business with the bank.

In May, the FDIC proposed tagging the largest banks with billions of dollars in extra fees to replenish the US government’s bedrock deposit insurance fund after it was tapped to backstop deposits above the $250,000 threshold. At the time, the regulator estimated the decision to cover all depositors at SVB and Signature cost the fund (i.e. US taxpayers) $15.8 billion.

FDIC Chairman Martin Gruenberg has previously said that at SVB the guarantee to uninsured depositors covered small and midsize business, as well as those with very large balances, and that the bank’s top 10 depositor accounts held $13.3 billion total. At least he wasn't lying.

As detailed by the FDIC document, we now know for a fact that in addition to serving a legion of startups and fledgling businesses, SVB was a go-to bank for tech industry giants, including some that have kept their relationships with the bank confidential.

Finally, Silicon Valley Bank and parent SVB Financial Group were both listed as having a combined $4.6 billion in deposits. SVB Financial has argued in its bankruptcy case that at least $2 billion in deposits the parent had with the bank should be returned. Federal regulators have said SVB Financial must apply to the bank’s receiver for that money.

While the regional banking crisis is currently on the backburner, it is nowhere near over: as long as the Fed continues its QT, the total amount of deposits in the financial system continues to shrink (it's why the Fed's BTFP program is so instrumental to avoiding an acceleration in the bank run).

In fact, once the small bank reserve constraint is hit again, expect round 2 of the 2023 banking crisis to hit with a vengeance.

It's why Peter Crane, president of money-fund tracking firm Crane Data LLC, said Friday at the Crane’s Money Fund Symposium in Atlanta that cash will "relentlessly" keep pouring out of banks and into money funds.

"Until they guarantee all deposits, which they will have to do at some point, institutional investors are looking at a big block of uninsured deposits” Crane said. “With cash, it’s the possibility of losing money you’re trying to avoid.”

On the retail side, Crane said that investors are shifting out of deposits because of the 4.5%-5% yield available in money funds relative to the sub-1% yield on bank deposits: “That’s the greed of a 4% spread,” he said. “You can drive a truck through that spread.”