Many were shocked (again) after the latest CPI and PPI data confirmed that the experts were once again dead wrong, and instead of the widely expected inflation tsunami, Trump's tariffs have so far sparked only continued disinflation (which will only become more acute as home prices slide). And yet, anyone who read our Beige Book analysis from April (not to mention our accurate prediction from last June that "The Experts Are All Wrong About Inflation Under A Trump Presidency") would have known just that: as we laid out, "Beige Book Finds Inflation Mentions Tumble To 3 Year Low" which was the clearest indication that despite the prevailing narrative, rising prices is simply not a thing businesses across the US are worried about. We got further confirmation of this last month, when the latest Beige Book found no runaway inflation (again) but instead that sentiment in the economy splitting along party lines.

Fast forward to today when the latest, July, Beige Book was released, and it revealed that according to reports across the 12 Fed districts, "economic activity increased slightly from late May through early July." Five Districts reported slight or modest gains, five had flat activity, and the remaining two Districts (New York and Philadelphia, naturally democrat strongholds) noted modest declines in activity. That, the Beige Book admitted, represented an improvement over the previous report, in which half of Districts reported at least slight declines in activity.

The Beige Book said that all Districts reported that while economic activity rebounded, uncertainty remained elevated, contributing to ongoing caution by businesses. Nonauto consumer spending declined in most Districts, softening slightly overall (hardly a signal of an imminent inflationary burst). Auto sales receded modestly on average, after consumers had rushed to buy vehicles earlier this year to avoid tariffs. Tourism activity was mixed, manufacturing activity edged lower, and nonfinancial services activity was little changed on average but varied across Districts.

Meanwhile, offsetting some of the economic slowdown, loan volume increased slightly in most Districts. On the flip side, construction activity slowed somewhat, constrained by rising costs in some Districts while home sales were flat or little changed in most Districts, and nonresidential real estate activity was also mostly steady. Activity in the agriculture sector remained weak. Energy sector activity declined slightly, and transportation activity was mixed.

Overall, the outlook was neutral to slightly pessimistic, as only two Districts expected activity to increase, and others foresaw flat or slightly weaker activity.

Focusing on labor markets, the Beige book reported the following:

As for prices, it should come as no surprise by now that the runaway inflation everyone was expecting just isn't there. Here is Beige book confirmation:

In short, for yet another month, the sky is not falling.

Here is a snapshot of highlights by Fed District:

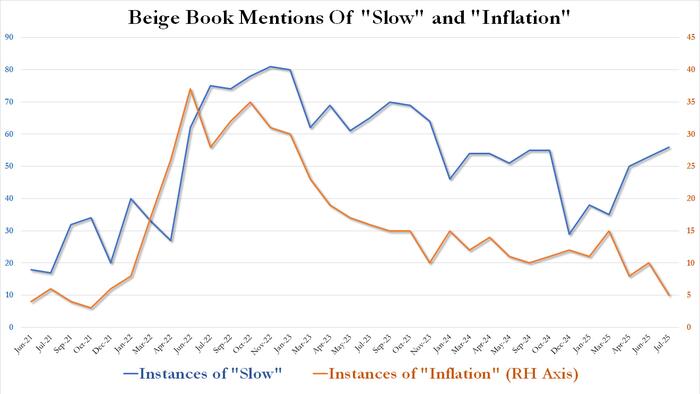

And finally, confirming that contrary to conventional wisdom the economic picture has been largely unchanged since April, the latest Beige Book found that contrary to prevailing media narratives, mentions of inflation actually dropped again, sliding to a new four year low of just 5 from 10 the previous month (effectively before the Biden inflationary explosion period) while mentions of "slow" rose to the highest since last October, just after the Powell Fed cut rates by 50bps. Overall, a very awkward report for a Fed that no longer has any excuse not to cut.

All of which suggests that the US economy - while hardly on fire as it was during the hyperinflationary period of Biden's admin - continues to chug along and is hardly collapsing as so many Trump foes would like to see; and it certainly is not seeing prices explode higher.