As BofA rates strategist Ralf Preusser writes in his weekly preview, "this week is one for the record book. We have not seen these three major central bank decisions (Fed, BoE, ECB); and key data releases (US ISM, payrolls, and the employment cost index, as well as Euro Area inflation, GDP, and confidence data) in the same week before. Not to mention in combination with month-end flow, which given the incidence of supply in Europe should be sizeable in both EUR and GBP."

DB's Jim Reid agrees writing that this week is set to be action packed for scheduled activity: "The main highlight is of course the FOMC conclusion (Wednesday), but the ECB and the BoE (both Thursday) will also likely hike. However, there's plenty of other events on the macro calendar, including the US jobs report on Friday, the flash CPI release from France and Germany (tomorrow), the Euro Area aggregate (Wednesday), regional and Euro Area Q4 GDP (tomorrow), global manufacturing (Wednesday) and services (Friday) PMIs/ISMs, China’s equivalents (tomorrow and Wednesday), US JOLTS (Wednesday), and US ECI (tomorrow)."

If that’s not enough, 12% of the S&P 500 by market cap report within a few moments of each other on Thursday night after the bell with Apple, Alphabet and Amazon the highlights in a busy week for earnings. Overall, a whopping 35% of S&P earnings by sector are set to report this week.

Going back to central banks, at the time of writing, the Fed is priced to deliver 26 bp, the ECB 50 bp, and the BoE 46 bp. BofA expects both the Fed and the ECB to deliver what is priced in, and sees a 25 bp hike from the BoE – marginally more likely than before after new lows in the PMIs – but risks are clearly skewed towards 50 bp.

DB's Reid adds that with a downshift to a 25bps Fed hike already priced in for Wednesday, the meeting will be all about what the Fed tone implies for further meetings. DB still think there'll be two more 25bps hikes after this one partly as the Fed won’t want to see financial conditions ease too much as a result of being too dovish.

Assuming central banks deliver on forwards, the key focus for the market will be the accompanying messages. The Fed’s message will likely be strongly influenced by critical data prints between now and Wednesday: PCE, ECI, ISM, JOLTS. And that message in turn risks looking dated already by the end of the week with ISM Services and NFP prints to come, also. Our economists remain hawkish relative to market pricing, expecting a terminal FF target range of 5.00-5.25% and the first cut not until Mar-2024, for which forwards price 100 bp more cuts than our colleagues expect.

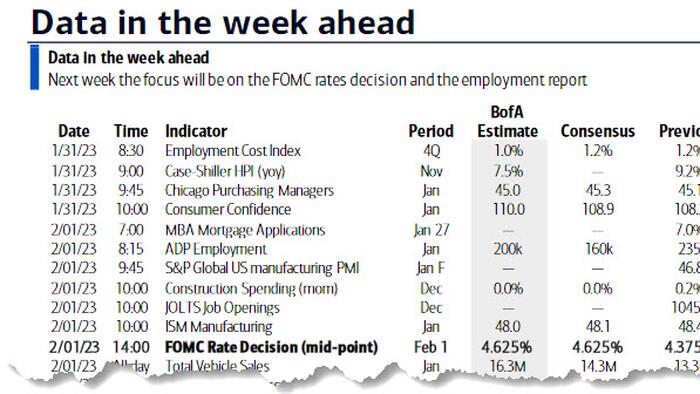

The last big and very important data point for the Fed before their meeting will be tomorrow’s Q4 ECI release (consensus 1.1% vs. +1.2% previously). Chair Powell is very focused on the relationship between core services ex-shelter inflation and wage pressures, with ECI near the top of their dashboard. JOLTS (Wednesday) is similarly important and may get a reference in the press conference.

Staying with labor markets, although Friday's employment report will come after the FOMC, it will as ever be a lightening rod for the market. For the headline, consensus is at +185k vs. +223K last month, and 3.6% for unemployment (DB also at 3.6%, vs. 3.5% last month). All eyes also on average hourly earnings and importantly the work week length which was soft last month hinting at a small crack in the labor market.

With regards to the ECB (Thursday), most economists expect another +50bps hike that would take the deposit rate to 2.50%. They also emphasize the importance of communicating expectations for the March meeting since core and underlying inflation remain sticky. The team sees further +50bps and +25bps hikes in March and May, respectively, and a terminal rate of 3.25%.

For the BoE decision that same day, DB economists differ with BofA and see another +50bps (vs 25bps) hike that will take the Bank Rate to 4%. That will potentially be the last 'forceful' hike in this tightening cycle. Although their view is that services and wages data warrant such a move, the risks are tilted to the downside. They continue to call for a 4.5% terminal rate as inflation pressures remain resilient.

European markets have lots of data to run through ahead of those decisions, with Eurozone Q4 GDP, inflation and labor market data all released early this week. Most of the key data will be out tomorrow, including Q4 GDP data for Germany, France, Italy and the Eurozone as well as CPI reports for Germany and France. Eurozone aggregates for the CPI and unemployment rate are released on Wednesday. DB economists expect Eurozone HICP to decline to 8.4% in January (vs 9.2% yoy in December) and continue falling to c.3.5% in Q4 this year. Core inflation is seen staying in a 5.0-5.5% range throughout first half of this year.

Finally, let's not forget about earnings, although that's impossible with a whopping 107 S&P companies reporting, including Apple, Amazon, Alphabet, Meta, Ford, AMD, Amgen, Qualcomm, Starbucks and dozens more.

Courtesy of DB, here is a day-by-day calendar of events

Monday January 30

Tuesday January 31

Wednesday February 1

Thursday February 2

Friday February 3

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the employment cost index on Tuesday, JOLTS job openings and ISM manufacturing on Wednesday, and the employment situation report on Friday. The February FOMC meeting is on Wednesday. The post-meeting statement will be released at 2:00 PM ET, followed by Chair Powell’s press conference at 2:30 PM.

Monday, January 30

Tuesday, January 31

Wednesday, February 1

Thursday, February 2

Friday, February 3

Source: DB, Goldman, BofA