A torrid, exhausting rollercoaster of a frenzied week full of central bank pauses and pre-pivots, a deluge of economic data and a third of the S&P500 reporting earnings including the world's largest companies, comes to a merciful close with Friday's nonfarm payrolls report.

As Newsquawk writes in its NFP preview, while the pace of payroll additions is expected to cool again in January, and while the unemployment rate is likely to have risen a little, tomorrow's print will still point to a tight labor market. Recent data has alluded to an easing in wage pressures, and this is likely to continue again in January, which will be received well by Fed officials. A continued decline here may give traders further confidence to price a path for rates more dovishly than the Fed’s current projections, and conversely, any upside surprise in the wages metrics may lead to a hawkish repricing of forward rates. Meanwhile, annual payroll benchmark revisions are difficult to predict, but some think that it will result in downward revisions to many of the prints in the second part of 2022.

CONSENSUS EXPECTATIONS:

DOWNWARD BIAS: There has been a suspicious propensity of the BLS numbers to come just above consensus expectations, with payrolls beating the median estimate on 7 of the past 8 reports (and 12 of the past 15). Will tomorrow make it a perfectly random 8 out of 9?

TIGHT LABOR MARKETS: Labor market proxies continue to allude to tight conditions; the weekly initial jobless claims data for the week that coincides with the establishment survey window declined vs the comparable week for the December data (192k vs 216k); continuing claims also declined (1.675mln vs 1.718mln). However, consumers themselves seem downbeat about the prospects for the labor market. The Conference Board’s gauge of consumer confidence for January said consumers’ assessment of present economic and labor market conditions improved at the start of the year, but expectations for the next six-months retreated, with consumers less upbeat about the short-term outlook for jobs, though their views for income prospects were more steady. Furthermore, the latest Challenger job cuts was remarkable in reporting a whopping 440% surge in corporate layoffs in January, with 102,943 cuts in the month, more than twice those announced in December and up 440% from January 2022. At some point the DOL will have to admit it is wrong in how it counts layoffs.

LABOR DEMAND: While analysts generally see labor market conditions as tight, some are pointing to signs of softening: S&P Global’s flash composite US PMI for January noted that jobs growth cooled in the month, with January seeing a far weaker increase in payroll numbers than evident throughout much of last year, which S&P said reflected a hesitancy to expand capacity in the face of uncertain trading conditions in the months ahead.” Some analysts also point to declining average workweek hours, which have been edging down from 34.6hrs at the beginning of 2022 and is expected to be unchanged at 34.3hrs in January – suggesting that aggregate hours worked in the labor force has been falling.

COOLING WAGES: With monetary policymakers firmly fixated on reducing inflationary pressures, there will again be attention on average hourly earnings figures. The rate of average hourly earnings is seen rising 0.3% M/M, matching December’s pace, although the annual measure is likely to fall to 4.3% from 4.6%, analysts predict. As a reference, the ADP's data revealed that the median change in annual pay for job-stayers was unchanged at 7.3% Y/Y, though the rate for job-changers rose 0.2ppts to 15.4%. And although it does not synchronize with this data release, the Employment Costs Index slowed for the third straight quarter in Q4, which will be a welcome sign for Fed officials who want to see wage growth cool; that said, employment costs themselves are still running at a rate of around 4.0% annualized; Wells Fargo said that while the ECI data further supports the argument for inflation moving back toward 2%, “labor cost growth remains too strong to be consistent with it staying there for the long-haul,” and the bank thinks that “more slowing will be needed before the FOMC feels comfortable declaring victory on inflation.”

PAYROLLS BENCHMARK REVISIONS: Annual benchmark revisions are also due to be made to the data series. This will impact both the Household and Establishment surveys. The household survey will include the annual population adjustment, which means that the household employment measure will not be directly comparable to prior months. Tomorrow’s report will also be accompanied by the annual benchmark revision to the establishment survey. The BLS’s preliminary estimate of the establishment survey revision suggested a 39k faster pace of monthly job growth on average from April 2021 to March 2022. Additionally, the 2022 immigration rebound suggests the possibility of a rise in tomorrow’s estimates of population, the labor force, and potentially the participation rate.

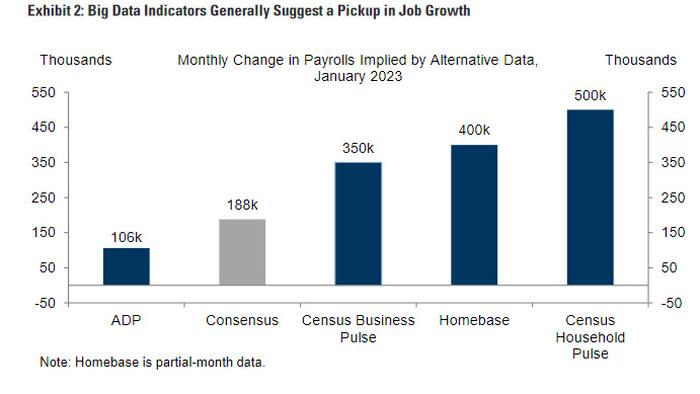

OUTLIER EXPECTATIONS: We should flag one potential market-moving forecast from Goldman, which estimates a blowout 300k payrolls surge in January, well above consensus of +190k, and here's why: "While consensus appears to expect the spike in corporate layoff announcements to weigh on tomorrow’s report, jobless claims have fallen further, and California WARN notices suggest the majority of these mass layoffs have not yet been implemented. Our well-above-consensus forecast also reflects strength in Big Data employment indicators, a boost from favorable seasonal factors that are spuriously fitting to last winter’s Omicron wave, still-elevated labor demand, and a 36k boost from the return of striking education workers. On the negative side, ADP’s employment data flagged possible disruptions from winter weather and California flooding."

ARGUING FOR A STRONGER-THAN-EXPECTED REPORT:

{kind=link}

ARGUING FOR A WEAKER-THAN-EXPECTED REPORT:

NEUTRAL/MIXED FACTORS:

BENCHMARK REVISIONS: Tomorrow’s report will be accompanied by the annual benchmark revision to the establishment survey. The household survey will include the annual population adjustment, which means that the household employment measure will not be directly comparable to prior months. Tomorrow’s report will also be accompanied by the annual benchmark revision to the establishment survey. The BLS’s preliminary estimate of the establishment survey revision suggested an upward adjustment of 462k to the level of March 2022 employment, which implies a 39k faster pace of monthly job growth on average from April 2021 to March 2022.

Needless to say, if the stronger-than-expected factors prevail, and if jobs magically come out far hotter than expected - say 300K or more - then much of the post FOMC meltup may whiplash lower as the "data dependent" Powell will not like to see a resurgence in the US labor market.

Source: Goldman