Commentary

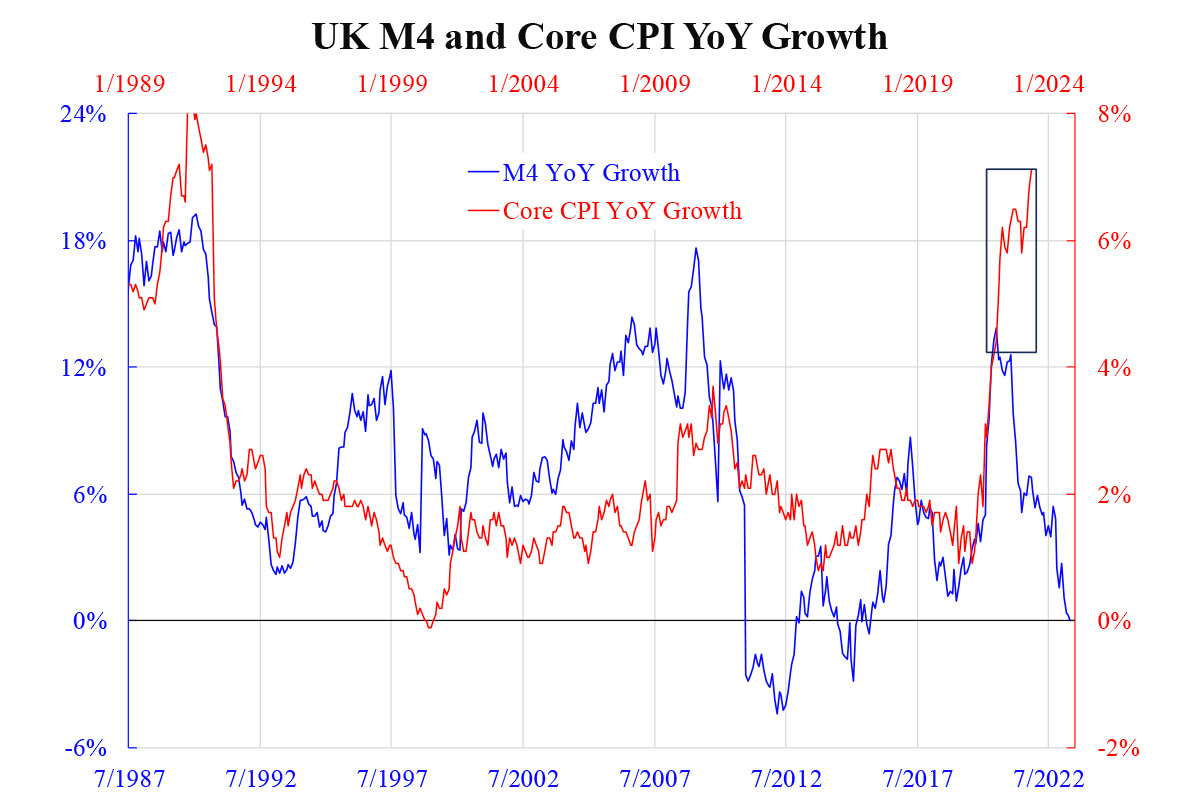

The nightmare for the central bank is not high inflation by itself but when high inflation is not responsive to tightening measures. As an example, we can look at the situation in the UK. The accompanying chart shows that the UK has broad money (M4) growing year-over-year (YoY) at zero percent, down from the recent peak of over 10 percent three years ago. Since broad money reflects not only the money in circulation but also its turnover rate, a sharp drop in growth should indicate that money flow (lending) is indeed cooling down.

(Courtesy of Law Ka-chung)How should this phenomenon, that lending is cooling while inflation is still heating, be interpreted? Notice that for the graph, we have already used core inflation, which excludes food and energy, so the volatile components and potentially the supply side shocks should be much reduced. The gap between broad money growth and inflation (price growth) is determined by real transactions (or roughly, real GDP) growth and money velocity growth. GDP growth should not be the reason, as it has recently slowed significantly to 0.2 percent.

Eliminating GDP growth indicates that money velocity growth explains the situation. Indeed, credit growth has been negative since mid-2022. But money velocity growth still being high means firms and households are not really borrowing (expanding the money supply) but transacting actively.

How can this be consistent with a sharp ease in real GDP growth? The answer lies in the uneven growth of GDP. Although secondary industry takes up less than 20 percent of the share while tertiary (services) takes up 70 percent, the former can be leveraged to boost GDP growth. Alternatively, as that 20 percent shrinks, the overall significant figure will be dragged down. UK manufacturing PMI has been under 50 since mid-2022 (again, for a year already), while services PMI remains above 53 and sometimes up to 56 over recent months. The answer should be evident by now.

Manufacturing activities are likely highly associated with lending, and both have been shrinking for a year. Services activities are not big transactions but are being conducted actively, thus increasing money velocity growth. Now the question boils down to how tightening policy can contain lending and real (mainly services) transactions. This is nothing more than asking people to put their money back in the bank rather than using it (for consumption).

The Bank of England (BoE) policy rate is now 5 percent while core inflation is 7 percent (the overall one even higher, near 9 percent). Putting money in a bank earns 5 percent (in fact, lower because banks offer a deposit rate of about 4 percent) but loses the purchasing power by 7 percent, that is, 2 percent real depreciation. Any rational agent would use it rather than save it. So, it is not the problem of money amount and lending (that contributes to broad money) but its price, which BoE still doesn’t understand.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.