Commentary

Silicon Valley Bank (SVB), the country’s sixteenth-largest bank with $209 billion in assets, failed on Friday in one of the most shocking developments to hit the banking sector since the global financial crisis fifteen years ago. SVB’s claim to fame was its deep connection to the venture capital and tech community of Silicon Valley, boasting that “44% of U.S. venture-backed technology and health care IPOs … bank with SVB.” Well, not anymore.

Is the broader banking sector at risk of contagion? This is the issue we need to look at as soon as possible.

SVB’s demise came suddenly (pdf). On Wednesday, the bank announced a loss of $1.8 billion from selling “available for sale” investment securities. Its holding company announced it would raise $2.25 billion to shore up the bank’s capital. Rather than comforting investors and depositors, this surprising announcement spooked them, “causing a run on the bank.” Within a few hours, depositors withdrew some $42 billion in cash, approximately 25 percent of total deposits, leaving the bank with a negative cash balance approaching $1 billion by the end of Thursday. Unable to shore up this shortfall overnight, the initially illiquid and then insolvent bank failed. California’s Commissioner of Financial Protection and Innovation took over the bank and appointed the FDIC as a receiver.

While the FDIC provides deposit insurance up to $250,000, representing less than 10 percent of SVB’s deposits. The vast majority of SVB’s $173 billion in deposits are uninsured. According to the FDIC, “uninsured depositors will receive a receivership certificate for the remaining amount of their uninsured funds.” These certificates will receive dividend payments from future sales of assets, which may not be enough for depositors to be repaid in full.

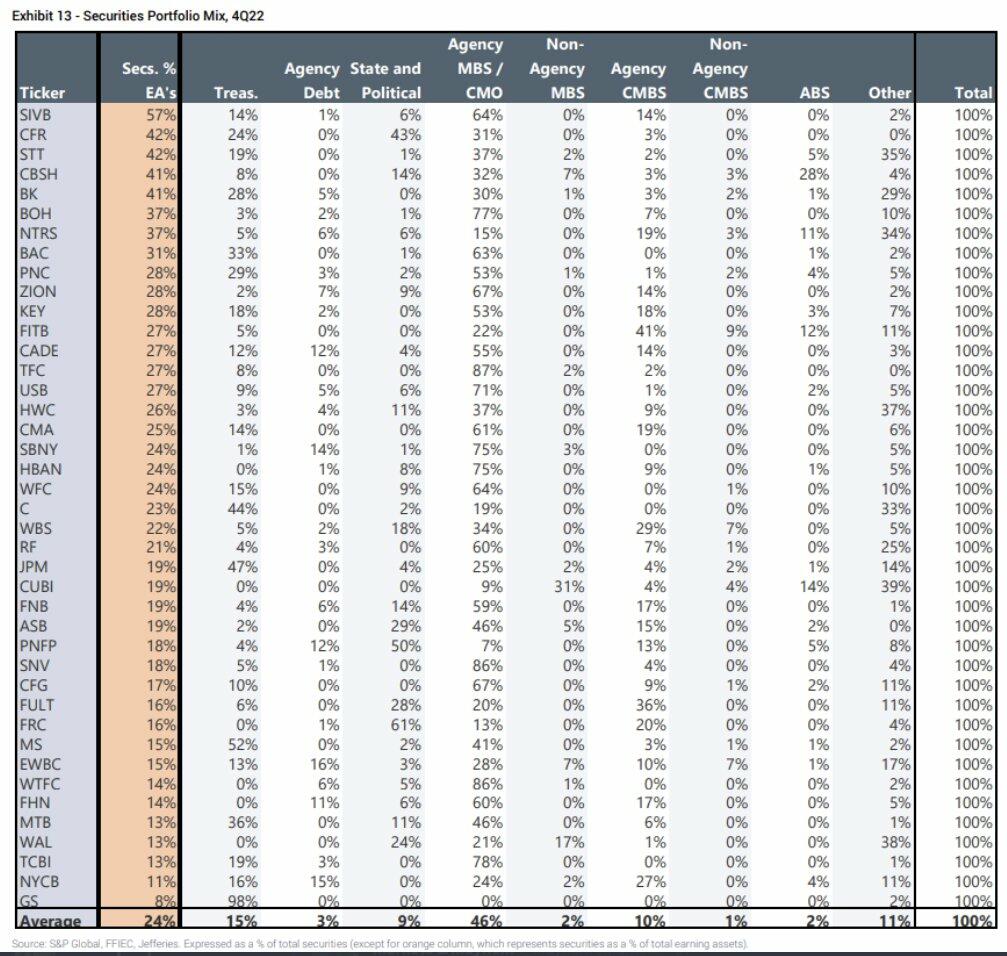

The issue for SVB was that its assets were heavily weighted to its investment portfolio. Specifically, some 57 percent of SBV’s assets were in marketable securities, primarily U.S. Treasury and mortgage-backed securities. With the rapid rise of interest rates over the past year, the market value of these bonds fell substantially. That fact won’t matter if a bank can hold these bonds until maturity when they will be repaid at par. But if a bank is suddenly forced to sell them to generate liquidity, i.e., to meet depositors’ demands for cash withdrawals, it is forced to sell them at a loss. A vicious circle ensues. Unplanned asset sales generate losses; losses weaken the bank’s financial position, and depositors get nervous and demand their money, requiring more assets to be sold, thereby stimulating further losses. As in the case of SVB, this can happen in days or even hours.

Illiquidity, not insolvency, typically causes banks to fail, which was undoubtedly true for SVB. The question now is, how many other U.S. banks are similarly exposed to this type of liquidity risk? Analysts are working overtime to review the data to see which other banks may be in a similar position to SVB. While SVB had the highest ratio of securities to assets, several other regional banks have more than a third of their holdings in similar categories. Should their depositors get nervous, bank runs could occur elsewhere in the coming days.

{kind=link}

The collapse of SVB has sent shockwaves through banking and financial markets. The NASDAQ Bank Index fell nearly five percent on Friday. Crypto has been particularly impacted, as SVB was a preferred bank for the industry. Two of the largest crypto exchanges, Coinbase and Binance, suspended the sale or convertibility of USDC, the stablecoin pegged 1:1 to the U.S. Dollar. As a result, USDC depegged and fell to $0.90 early on Saturday. With USD 41 billion in circulation, this represents an unrealized loss of over $4 billion. Coinbase’s parent Circle confirmed on Saturday that it had $3.3 billion of reserves at SVB that it could not get out of the bank on Thursday. This situation represents a new challenge to the viability of the stablecoin model.

At a minimum, readers should take this opportunity to consider whether their banks are safe and sound and where they may face unknown risks. But that’s not enough. Banking crises are often driven by human nature and psychology as much as asset and liability mismatches. Should investors and depositors gain confidence that the issues at SVB were bank-specific in the coming days, perhaps this storm will pass. However, fear is a highly contagious pathogen. To the extent that a broader panic ensues, we may be looking at a frightening banking and financial markets crisis. Keep a close eye on this one over the coming days.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.