The IRS has announced the annual inflation adjustments for the year 2026, including tax rate schedules, tax tables and cost-of-living adjustments.

These are the official numbers for the tax year 2026—the tax year that begins on January 1, 2026. These are not the numbers that you’ll use to prepare your 2025 tax returns in 2026 (you’ll find those official 2025 tax numbers here). These are the numbers that you’ll use to prepare your 2026 tax returns in 2027—and that you’ll use for your tax planning throughout the year.

If you aren’t expecting any significant changes in 2026, you can use the updated numbers to estimate your liability. If you plan to make more (or less) money or change your circumstances—including getting married, starting a business, or having a baby—consider adjusting your withholding or tweaking your estimated tax payments.

One quick note: In addition to these announced changes, don’t forget that there have been several significant changes to the tax code, thanks to the One Big Beautiful Bill Act (OBBBA). You’ll see some of those referenced below. You may want to make changes to your withholding when the new withholding tables are published—those will be effective beginning in 2026 (there are no changes for 2025).

There are seven (7) tax rates in 2026. They are: 10%, 12%, 22%, 24%, 32%, 35% and 37% (there is also a zero rate). These rates, which were lowered as part of the Tax Cuts and Jobs Act (TCJA), were made permanent under OBBBA.

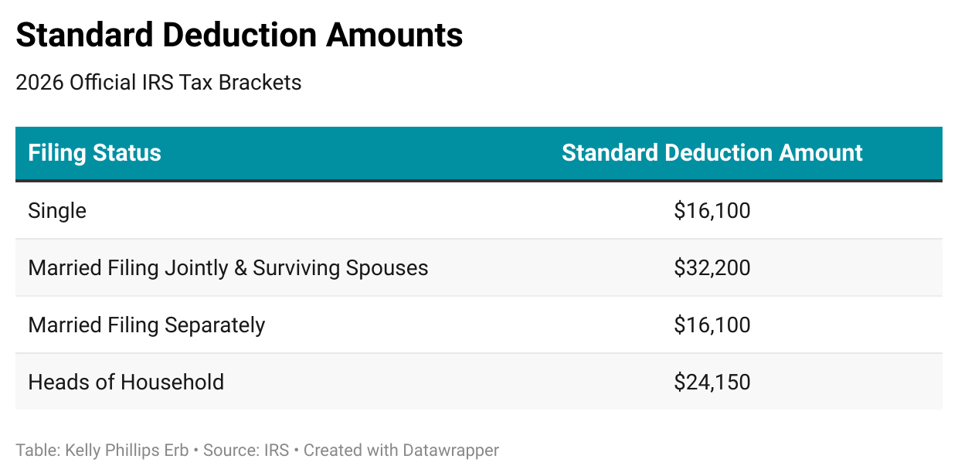

Here's how those break out by filing status:

It’s worth noting that in the official Rev. Proc. charts, there are discrepancies in the numbers for Heads of Household (HOH). Notably, in the Rev. Proc. for HOH, the 24% rate ends with $201,775 but the 32% rate begins at $201,751. I’ve reached out to the IRS and will update accordingly.

Your marginal tax rate determines what you pay when you receive the next dollar of income—it represents the highest tax rate you pay for the year. For the tax year 2026, the top tax rate is 37% for individual single taxpayers with incomes greater than $640,600 ($768,700 for married couples filing jointly).

The other rates are:

There will be no personal exemption amounts in 2026. Personal exemptions used to decrease your taxable income before you determined the tax due. You were generally allowed one exemption for yourself (unless you could be claimed as a dependent by another taxpayer), one exemption for your spouse if you filed a joint return, and one personal exemption for each of your dependents—but that's no longer the case thanks to the 2017 and 2025 tax laws.

The standard deduction amounts will increase to $16,100 for individuals and married couples filing separately, representing an increase of $350 from 2025 (this isn’t just an inflation adjustment—OBBBA increased the standard deduction amounts). Married couples filing jointly will see a deduction of $32,200, a boost of $700 from 2025, while heads of household will see a jump to $24,150, an increase of $525 from 2025.

For 2026, the additional standard deduction amount for the aged or the blind is $1,650 (up from $1,600 in 2025). The additional standard deduction amount increases to $2,050 for unmarried taxpayers (an increase of $50 from 2025).

For 2026, the standard deduction amount for an individual who may be claimed as a dependent by another taxpayer cannot exceed the greater of $1,350 or the sum of $450 and the individual’s earned income (not to exceed the regular standard deduction amount).

The kiddie tax applies to unearned income for children under the age of 19 and college students under the age of 24. Unearned income is income from sources other than wages and salary, like dividends and interest.

Your child must pay taxes on their unearned income in 2026, but if that amount is more than $1,350 but less than $13,500, you may be able to elect to include that income on your return rather than file a separate return for your child. These are the same numbers as in 2025.

The same “regular” rules apply to earned income.

As a result of OBBBA, the maximum amount of the child tax credit in 2026 is $2,200. The amount used to determine the amount of the credit that may be refundable is $1,700.

In 2026, the maximum Earned Income Credit (EIC) amount is $8,231 for qualifying taxpayers who have three or more qualifying children, up from $8,046 for tax year 2025. Income thresholds and phaseouts apply.

In 2026, the maximum amount of employer-provided childcare tax credit has increased from $150,000 to $500,000 ($600,000 if the employer is an eligible small business). That’s not a typo—as with the standard deduction, this isn’t just an inflation adjustment, it was increased thanks to OBBBA.

For 2026, the maximum adoption credit for adopting a child is the amount of qualified adoption expenses up to $17,670—up from $17,280 in 2025. For tax year 2026, the amount of credit that may be refundable is $5,120.

The AMT exemption rate is also adjusted for inflation. The AMT exemption amount for tax year 2026 for single filers is $90,100 and begins to phase out at $500,000 (in 2025, the exemption amount for single filers was $88,100). In 2026, the AMT exemption amount for married couples filing jointly is $140,200 and begins to phase out at $1,000,000 (in 2025, the exemption amount for married couples filing jointly was $137,000).

Capital gains rates will not change for 2026, but the brackets for the rates will change. Most taxpayers pay a maximum 15% rate, but a 20% tax rate applies if your taxable income exceeds the thresholds set for the 37% ordinary tax rate. Exceptions also apply for art, collectible, and section 1250 gain (related to depreciation). The maximum zero rate amounts and maximum 15% rate amounts break down as follows:

For 2026, the $2,500 maximum deduction for interest paid on student loans—called qualified education loans—will begin to phase out for taxpayers with modified adjusted gross income above $85,000 ($175,000 for joint returns) and will completely phase out for taxpayers with modified adjusted gross income of $100,000 or more ($205,000 or more for joint returns).

Educational assistance programs (which now include employer payments on student loans) are the equivalent of free money offered by employers and are considered fringe benefits to employees. Fringe benefits are usually taxable to employees and must be included in pay – unless they’re specifically excluded by law. Fortunately for taxpayers, educational assistance benefits are excluded so long as they meet certain qualifications. For 2026, the maximum exclusion amount is $5,250.

For the 2026 tax year, the phaseout amount for the Lifetime Learning Credit begins when adjusted gross income (AGI) reaches $80,000 for single taxpayers (it’s completely phased out at $90,000) while the phaseout amount for married taxpayers filing jointly begins at $160,000 (it’s completely phased out at $180,000). Those amounts are not adjusted for inflation.

In 2026, the amount of the eligible educator deduction allowed in connection with books, supplies (other than nonathletic supplies for courses of instruction in health or physical education), computer equipment (including related software and services) and other equipment, and supplementary materials used by the eligible educator in the classroom is $350 (an increase of $50 from 2025).

As part of the 2017 tax reform law, sole proprietors and owners of pass-through businesses like LLCs, S corporations, and partnerships may be eligible for a qualified business income (QBI) deduction of up to 20% to lower the tax rate for qualified business income (this is the same percentage as in 2025, thanks to OBBBA). The deduction is subject to threshold and phased-in amounts.

In 2026, OBBBA also adds a minimum section 199A deduction of $400. A taxpayer will be required to have a minimum of $1,000 of qualified business income to be eligible for the deduction.

Under OBBBA, reporting thresholds for Form 1099-MISC (for payments not covered by other 1099 forms), and Form 1099-NEC (for nonemployee compensation) have increased to $2,000 in 2026, down from $600 in 2025. You can find out more about the changes here.

In 2026, the monthly limitation for the qualified transportation fringe benefit and the monthly limitation for qualified parking increases to $340, an increase of $15 from 2025.

Health Savings Accounts (HSA). In 2026, the annual contribution limitation for an individual with self-only coverage under a high deductible health plan (HDHP) will be $4,400 ($8,750 for a family). At age 55, individuals can contribute an additional $1,000.

Medical Savings Accounts (MSA). For 2026, a high-deductible health plan (HDHP) is one that, for participants who have self-only coverage in an MSA, has an annual deductible that is not less than $2,900 (an increase of $50 from 2025) but not more than $4,400 (an increase of $100 from 2025). For participants with family coverage, an annual deductible that is not less than $5,850 (a boost from $5,700 in 2025) but not more than $8,750 in 2026 (up from $8,550 in 2025). For self-only coverage, the maximum out-of-pocket expense amount is $5,850 in 2026, an increase of $150 from 2025. For family coverage in 2026, the maximum out-of-pocket expense amount is $10,700 in 2026, an increase of $200 from 2025.

Health Flexible Spending Cafeteria Plans. For 2026, the dollar limitation for voluntary employee salary reductions for contributions to health flexible spending arrangements increases to $3,400, up $100 from prior year. For cafeteria plans that permit the carryover of unused amounts, the maximum carryover amount is $680, an increase of $20 from 2025.

The unpopular shared individual responsibility payment is eliminated for the tax year 2026 (as it was in 2025).

Looking for retirement numbers for IRAs (including Roth IRAs) and qualified plans? We’ll link to those once the IRS has made them available.

In 2026, the foreign-earned income exclusion amount is $132,900, up from $130,00 in tax year 2025.

The federal estate tax exclusion for decedents dying will increase to $15,000,000 per person (up from $13,990,000 in 2025) or $30,000,000 per married couple in 2026 (up from $27,980,000 in 2025). As with some of the other adjustments, this increase is related to changes in OBBBA.

The federal gift tax exclusion remains $19,000 in 2026, the same as 2025. That means you can gift $19,000 per person to as many people as you want with no federal gift tax consequences in 2026; if you split gifts with your spouse, that total is $38,000. If your spouse is not a U.S. citizen, tax-free gifts are limited to present interest gifts whose total value is below the annual exclusion amount, which is $194,000 in 2026 (it was $190,000 in 2025).

Some itemized deductions found on Schedule A have also changed under the OBBBA. Here’s a look at some of the most common itemized deduction:

For those high-income taxpayers who itemize their deductions, the Pease limitations, named after former Representative Don Pease (D-OH) used to cap or phase out certain deductions. The TCJA eliminated the Pease limitations and that was made permanent by OBBBA. However, there is a new limitation on the tax benefit from itemized deductions for those taxpayers in the highest tax bracket (37%) which effectively caps the benefit for those deductions at 35%.

What about those new tax deductions under OBBBA, including those for tipped and overtime workers? Those deductions, reported on a new Schedule 1-A, are largely referred to on the schedule by their popular monikers: No Tax on Tips, No Tax on Overtime, No Tax on Car Loan Interest and the “Enhanced Deduction for Seniors.”

For more on Schedule 1-A, including phaseouts, click here.

These are the official numbers published by the IRS. You can compare these numbers to the 2026 Bloomberg projections here.

You can read all of the official IRS numbers in Revenue Procedure 2025-32.